Prompt response rule

Statutory Provisions

[Sec. 319(b)]: This rule applies to any “covered financial institution,” a term that, as we pointed out earlier, includes insured and commercial banks, credit unions, and thrift institutions, among others. If a covered financial institution receives a request from its appropriate federal banking agency and the request relates to anti-money laundering compliance by the institution, or one of its customers, the institution must supply information and account documentation for any account opened, maintained, administered, or managed in the United States and must do so within 120 hours of receiving the request.

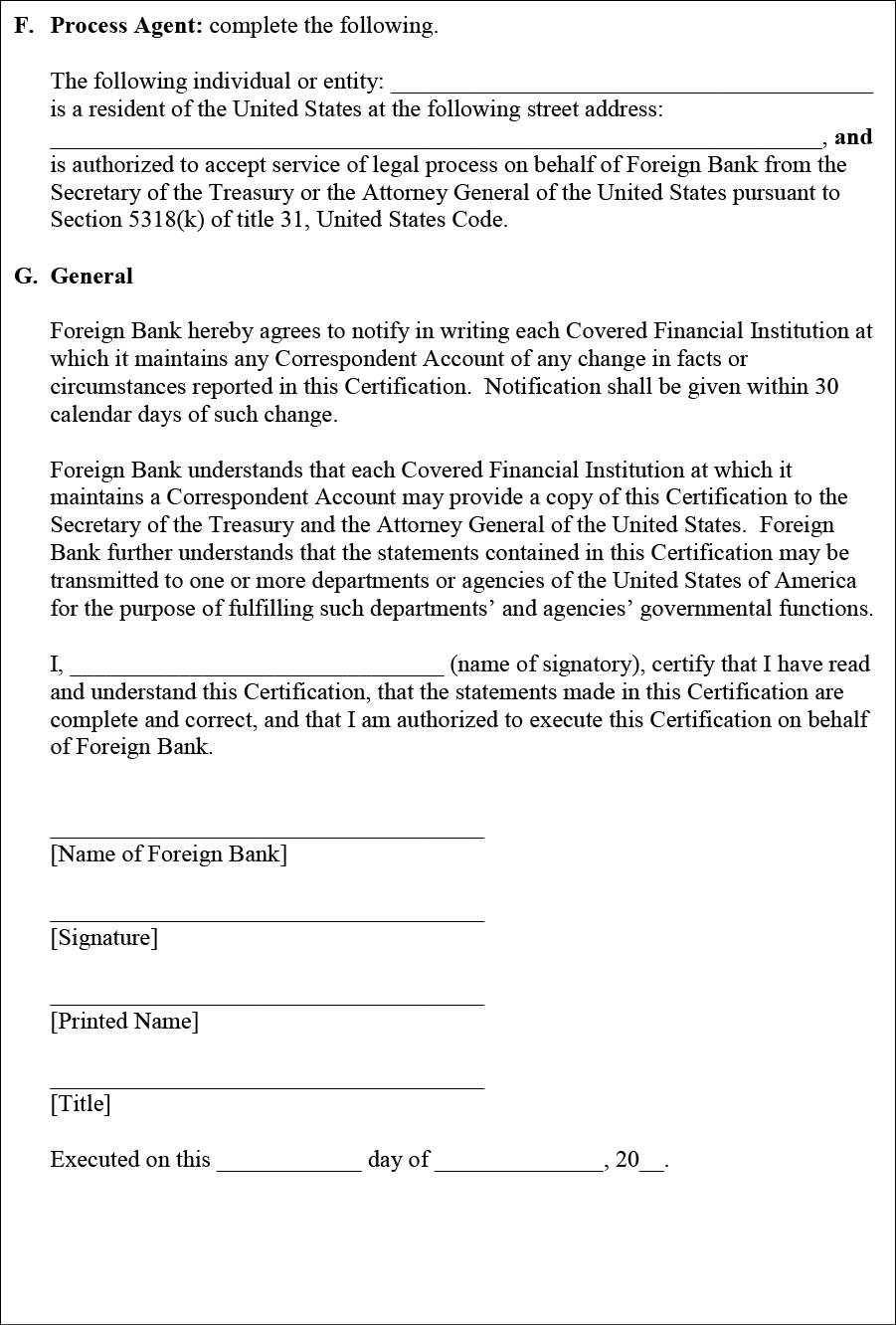

Also, a covered institution that maintains a correspondent account in the United States for a foreign bank is required to maintain records identifying the owners of the foreign bank and the name and U.S. address of a person authorized to accept service of process for records on the account.

A covered financial institution is also required to close a correspondent account of a foreign bank held in the U.S. within ten business days after receiving notice from the Secretary of the Treasury or the Attorney General. This provision includes a liability shield for the institution closing the account and it includes a penalty for an institution that does not comply.

Financial institutions have 60 calendar days after enactment (October 26, 2001) to comply with these requirements.

Regulatory Provisions

As we pointed out earlier, FinCEN has issued regulations in connection with Section 319(b), which we just described, and Section 313, which we described earlier. Here’s a summary of what they say:

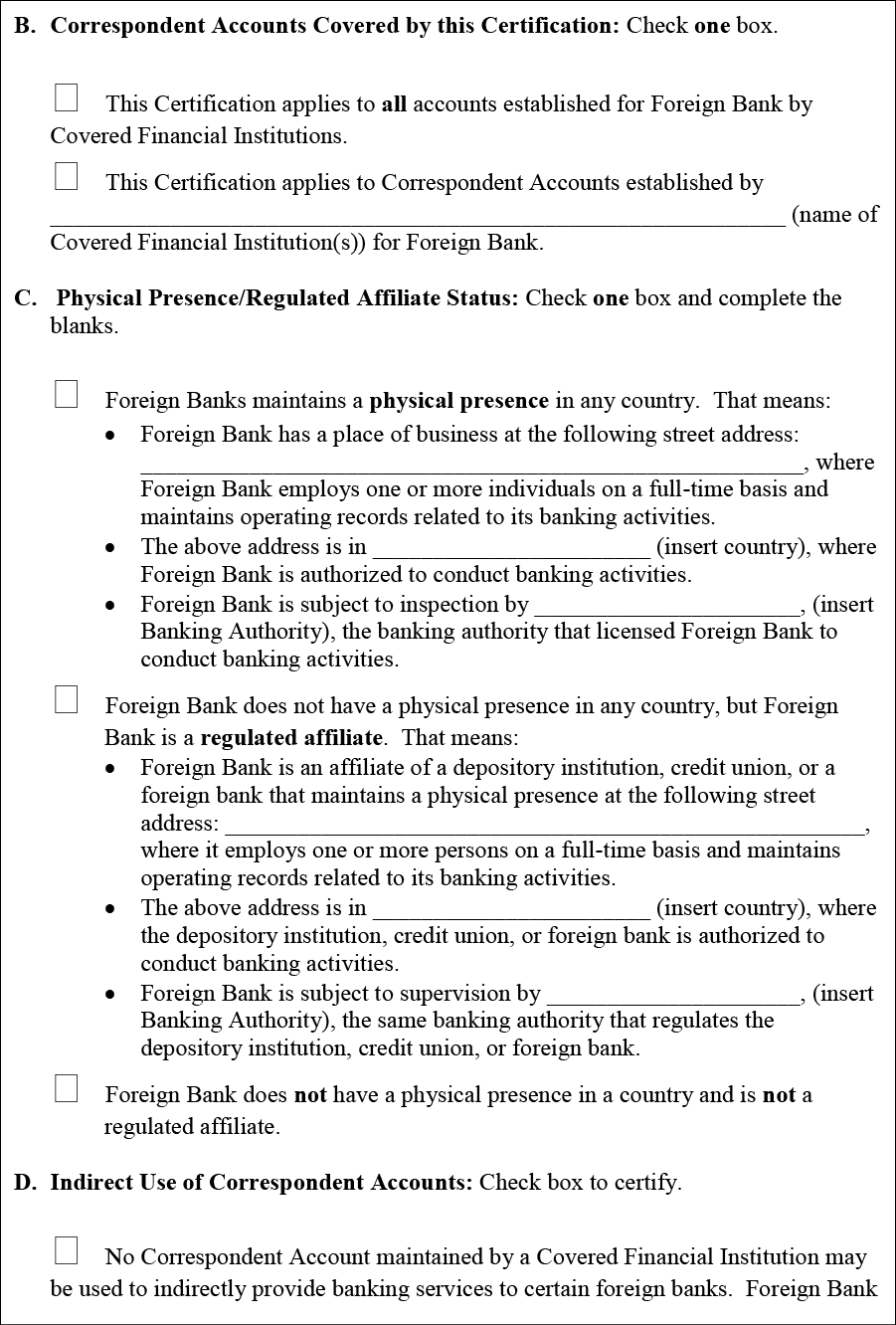

First, a covered financial institution is prohibited from opening or holding a correspondent account for a “foreign shell bank,” which is defined as a foreign bank without a physical presence in any country. [31 CFR 1010.605(g)and 31 CFR 1010.630(a)] A foreign bank is a bank organized under foreign law, or an agency, branch or office located outside the United States of a bank. [31 CFR 1010.100] This rule allows, however, the covered financial institution to hold a correspondent account for a regulated affiliate of the covered financial institution. [31 CFR 1010.630(a)]

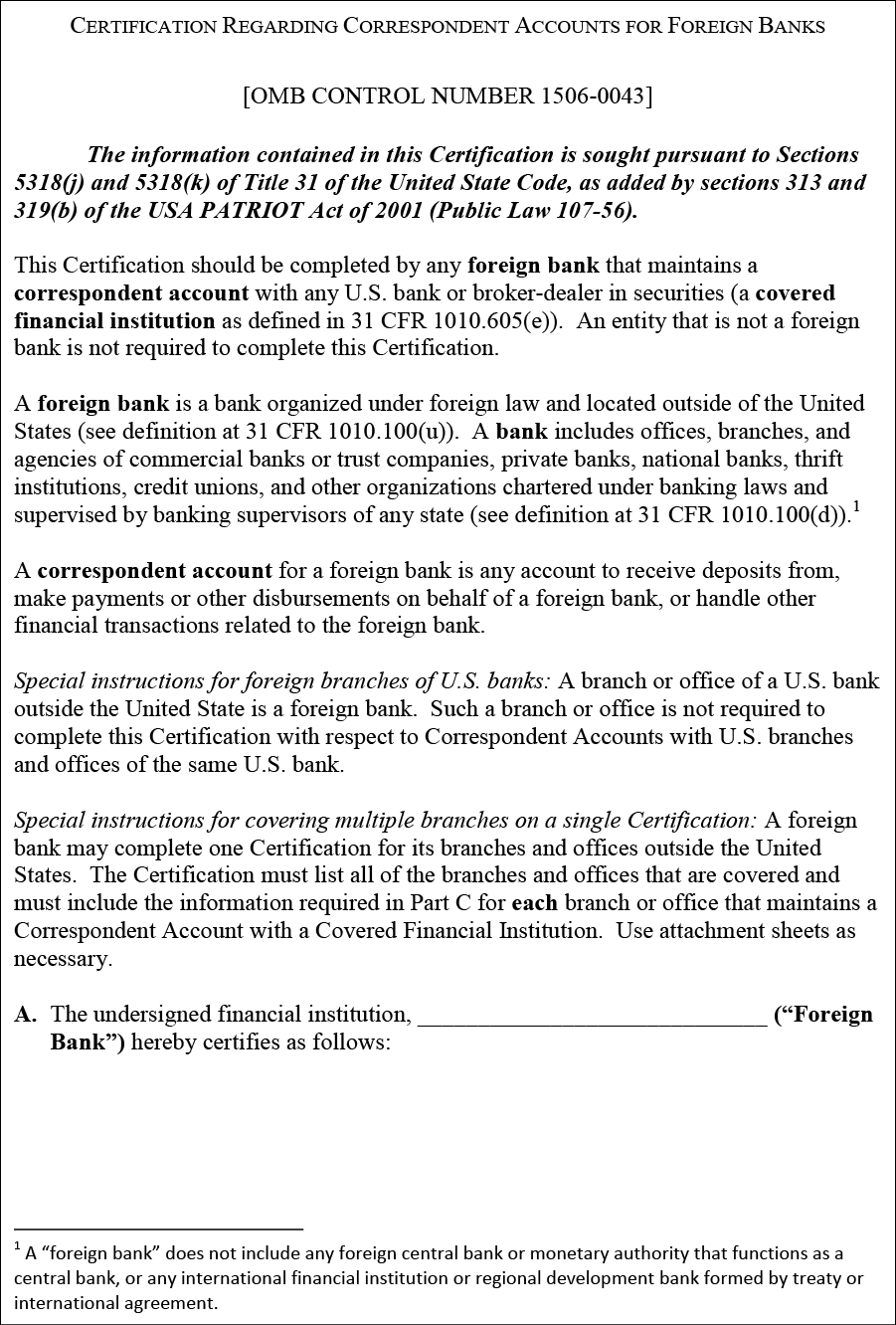

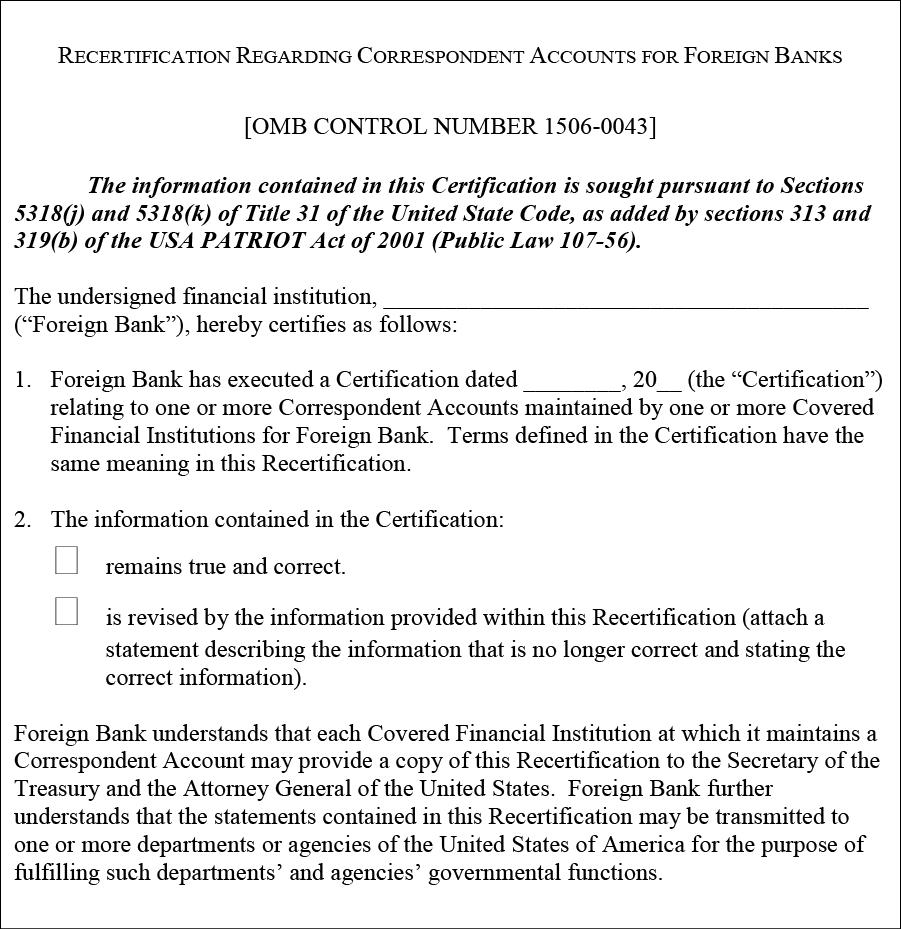

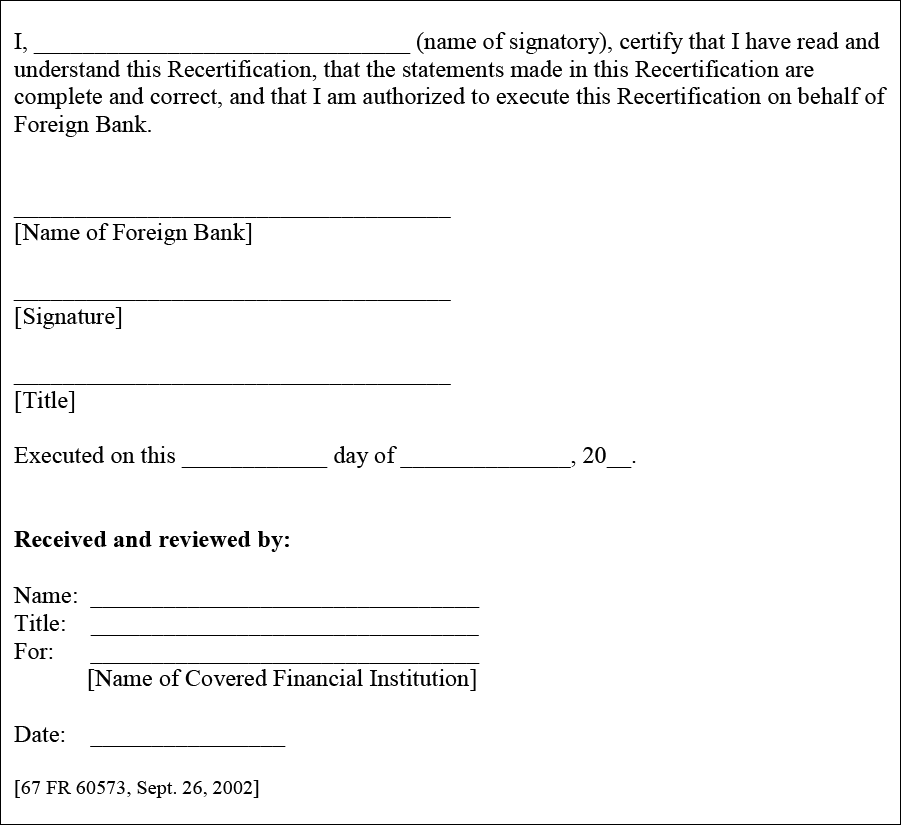

Second, a covered financial institution must take steps to make sure that a correspondent account with a foreign bank is not being used as an account for a foreign shell bank. [31 CFR 1010.630(a)] The covered financial institution can do this by having the foreign bank certify or recertify at least every three years the information the foreign bank is asked to supply on a FinCEN form. The FinCEN form is either the regulation’s Appendix A for certifications or Appendix B for recertifications. The form asks for information concerning the foreign bank, such as the address of its physical presence, or that it has no physical presence but is a regulated affiliate, etc. We have reprinted the text of these certification forms at the end of this section.

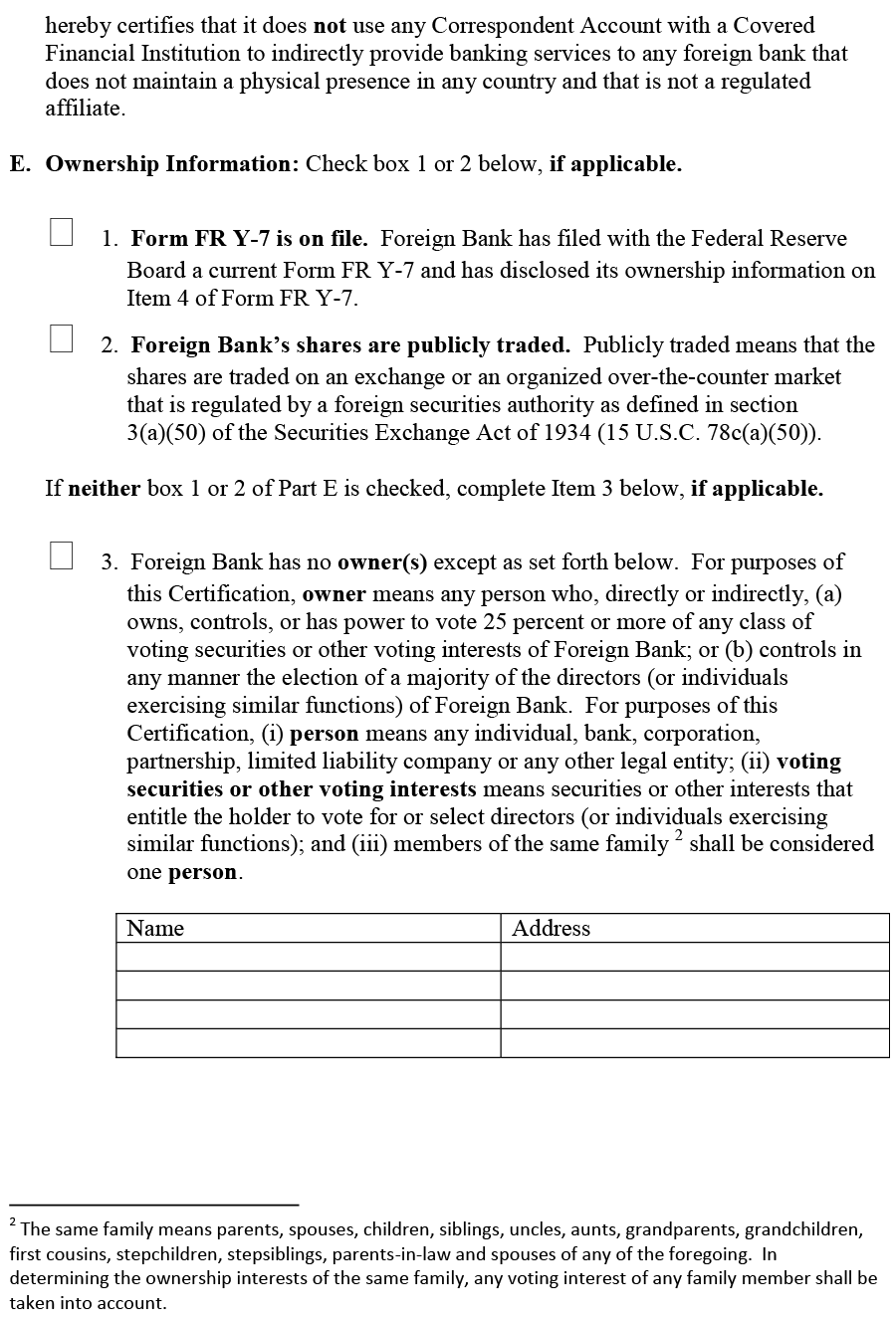

Third, a covered financial institution must maintain records concerning any correspondent account held for a foreign bank. The information in the records must identify “the owners of each such foreign bank whose shares are not publicly traded and the name and street address of a person who resides in the United States and is authorized, and has agreed to be an agent to accept service of legal process for records regarding each such account.” [31 CFR 1010.630(a)] The certification forms mentioned in the previous paragraph request this information from the foreign bank.

Fourth, a covered financial institution has an ongoing obligation with respect to the certifications. The rule says that if the institution “knows, suspects, or has reason to know” that the information in the certification is not correct, the institution must either request accurate information from the foreign bank or attempt to verify the information in some other way. [31 CFR 1010.630(c)] This starts the clock moving. If the foreign bank does not verify or correct the information or the covered financial institution cannot verify it by other means within 90 calendar days of starting the verification attempt, the covered financial institution must close all correspondent accounts with that foreign bank and the closing must be complete within a “commercially reasonable time.” [31 CFR 1010.630(d)]

Fifth, a covered financial institution that holds a foreign bank correspondent account that exists on October 28, 2002, must obtain and verify the required information by March 31, 2003. Otherwise, the institution must close the account within a commercially reasonable time after March 31, 2003. [31 CFR 1010.630(d)] For other foreign bank correspondent accounts (those established after October 28, 2002), the covered financial institution must obtain the certification within 30 calendar days after opening the account or close all correspondent accounts with that foreign bank within a commercially reasonable time. [31 CFR 1010.630(d)] A foreign bank whose correspondent account is closed under these rules must provide new certifications in order to open a new correspondent account with the covered financial institution. [31 CFR 1010.630(d)]

Finally, the covered financial institution must keep all certifications and any documents accompanying the certifications for at least five years following the date that a foreign bank has no correspondent accounts with the covered financial institution. [31 CFR 1010.630(e)]

Text of the certification form and the recertification form

As we mentioned above, a covered financial institution must obtain certain certifications from foreign banks for which the covered financial institution maintains correspondent accounts. The certification and recertification forms for correspondent accounts for foreign banks are located on FinCENs website http://www.fincen.gov/ [12 CFR 1010.605(b)] (Click on the Depository Institutions Home link)

Responding to a federal government request or notice

The regulation requires a covered financial institution to respond promptly to a request from a federal government law enforcement entity when it requests information collected under the rules we’ve described above. In particular, the covered financial institution must provide the information within seven days after the institution receives the request. The covered financial institution must also close a foreign bank correspondent account if it receives notice from the Secretary of the Treasury or the Attorney General that the foreign bank has not responded to a subpoena or summons. [31 CFR 1010.670(c)] Failing to terminate an account under these rules could subject the covered financial institution to civil penalties of up to $10,000 per day while in violation. [31 CFR 1010.670(d)]