| December 2020 |

Note: Discontinuing Support for Internet Explorer 11

(IE11) Internet Explorer 11 will no longer

be a supported browser in Q2 of 2021, most likely

with the April Production release. Our recommended

browser for accessing the application(s) will

continue to be, Google Chrome, and going forward

as of Q2 next year will also be Microsoft Edge

(Chromium based, version 79.0.309 or

newer). Wolters Kluwer does not anticipate

prevalent issues for users accessing the

application(s) via IE11, however, after the April

Production release, we will no longer remediate

reported bugs that are specific to the IE11

browser.

New Functionality

- URLA

- Starting January 1, 2021, the revised Uniform Residential Loan Application can be used

instead of the Fannie Mae 1003 Freddie Mac 65

Universal Residential Loan Application. If your

institution wants to use the revised application

form during the early adoption period, select the

Early adopt URLA option in Administration.

Selecting this option will not impact existing

transactions.

Set a reminder on your calendars

now to update Administration only after January 1,

2021. Testing can occur before this date on

Customer Test. Note:

- Do not select Early Adopt

URLA in Administration prior to 01/01/2021.

- For organizations not using the revised URLA

until the mandatory date, the Early adopt

URLA option should not be selected in

Administration.

On the Application page, select

URLA for the revised Uniform Residential

Loan Application or UCA-RE for the Credit

Application Real Estate for the Select your credit

application option. The selected document will

display on the Document Data and Print

pages. The default selection for Select

you credit application depends on the document

policy. If the Select the Fannie Mae 1003

Freddie Mac 65 Uniform Residential Loan

Application (URLA) is selected for a document

policy, URLA will default as selected. If

Select the Fannie Mae 1003 Freddie Mac 65

Uniform Residential Loan Application (URLA) is

not selected, UCR-RE will default as selected. The

default value can be changed at transaction

time.

- For Help information about using the new URLA,

select Application.

- We will continue making improvements prior to

the 3/1/2020 regulatory date. If you have any

feedback for us, please let us know.

- WK E-Sign

- When Parallel Signing and more than one

recipient are selected, Package Information will

not display because this information is not needed

for parallel signing.

Note: To use Parallel Signing, confirm each

recipient has selected Smart Consent in WK

E-Sign prior to sending a package to that

recipient. To confirm and view the status for

each recipient, complete one of the following:

- Log in to Group Admin under Support. Select

Users and Find. Their profile will

display their status.

- Search for and select a user on the Home page.

Their profile will display their status.

- If you are licensed for WK E-Sign, you can now

display all the generated documents from any

package for the Application or Closing Phase.

Select Display all generated document

packages after selecting the Package in the

Phase drop-down list on the Print page.

-

Lender Documents and Content

Due to technical issues, several licensed lender

documents and content were introduced with our

November 2020 updates. The introduction was

recently discovered and has been corrected to

remove the licensed lender documents and content.

The additional content should not affect the

enforceability of any documents and is essentially

a non-required, over-disclosure.

- Loan Product Advisor and Desktop Underwriter

- The Loan Product Advisor and Desktop

Underwriter have been updated to support the early

adoption period of the revised URLA. If

URLA is selected for Select your credit

application on the Application page,

application information will be sent to the

third-party services in Mismo 3.4 format as

required by Freddie Mac/Fannie Mae

specification.

|

| November 2020 |

Note: Wolters Kluwer offices will be closed on Thanksgiving and

the following day (11/26 and 11/27).

Note: Discontinuing Support for Internet Explorer 11

(IE11) Internet Explorer 11 will no longer

be a supported browser in Q2 of 2021, most likely

with the April Production release. Our recommended

browser for accessing the application(s) will

continue to be, Google Chrome, and going forward

as of Q2 next year will also be Microsoft Edge

(Chromium based, version 79.0.309 or

newer). Wolters Kluwer does not anticipate

prevalent issues for users accessing the

application(s) via IE11, however, after the April

Production release, we will no longer remediate

reported bugs that are specific to the IE11

browser.

New Functionality

- Application

- The Title column has been added to the

Property section. Specify is the default entry in

the column. Select Specify to open a dialog

box and complete the following information: Title

Will Be Held in What Name(s), Use Collateral

Owners, Describe How Title Will Be Held and

Description, and Estate Will be Held in. After

saving the entered information, Specify changes to

View. Select View to make changes. This

information will print to the Fannie Mae 1003

Freddie Mac 65 Universal Residential Loan

Application or Credit Application Real Estate

documents.

- Previously, the Present Housing Expenses

section did not populate when a party was added to

a transaction created from a template. This issue

has been resolved, and the Present Housing

Expenses section will include the data.

- Parties

- In preparation for the Revised URLA effective

in 2021, the Parties page has been updated to

include Country and Unit # in the

Employer Information section for both borrowers

and cosigners. These fields are applicable for

current, additional, and previous employment types

on the new URLA.

- Financial Analysis

- The Property Type field in Real Estate Owned

section was converted to a drop-down list with

additional values to accommodate Desktop

Underwriter and Loan Product Advisor requirements.

If the real estate owned collateral is tied to a

collateral item, a value will be defaulted when

applicable. These values will print to the Fannie

Mae 1003 or the UCA-RE.

- Important Notice: WK E-Sign Parallel Signing

- In a future release, when Parallel

Signing is selected and more than one

recipient is selected, Absolute Expiration

Date and the grid displaying Package Type,

Description, and Default Business…/Abs Exp.

Date… will not display. This information is

not used for parallel signing. Until Absolute

Expiration Date is removed, ignore this

section when sending a package using parallel

signing, and your package will not expire to

paper.

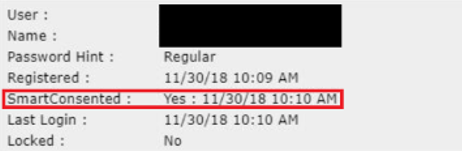

- Verify Smart Consent prior to sending a

Parallel Signing package: To avoid violating

ESign/UETA rules, your financial institution

should monitor each party's consent prior to

sending to the parallel signed package to WK

E-Sign. Prior to sending a package in WK E-Sign,

confirm that each recipient has selected Smart

Consent.

To confirm that each recipient has

used Smart Consent before sending a package to WK

E-Sign:

- An Administration user should log into Group

Administration.

- Under Support, enter an email address under

Find. After finding the user, their profile will

show their consent status. You can also search for

the user on the Home page. After selecting the

user, their consent status will display.

- Administration

- In Administration on the Indexes tab,

information entered in the Source field for a

user-defined index will populate the Adjustable

Rate Mortgage Disclosure Conventional, and

Adjustable Rate Mortgage Program Disclosure when

the user-defined index is selected in

Calculations.

-

Previously, loan originator information was

manually entered on the Document Data page. Now,

the information entered in the Title,

Email, and License ID fields when

setting up a Loan Officer on the Contacts tab in

Administration will automatically populate on

documents including this information.

|

| October 2020 |

What's New

New Functionality

- Application Page

-

In an effort to prepare you for URLA revisions

effective in 2021, we are releasing the

Application page feature now. This page is modeled

after the URLA revisions. We hope this can help

you prepare your staff between now and the

effective date, so the URLA revision is not a

major event for your institution.

The Application page is now available as the

first tab on each transaction and when using OLA,

you will now be directed to Application instead of

Parties when opening your inquiry. The purpose of

this page is to gather the borrower-related

information required to complete an application.

Until the revised URLA is released, this page can

be used to complete the Fannie Mae 1003/Freddie

Mac 65 Universal Residential Loan Application or

Credit Application Real Estate documents.

The Application page contains the following

sections:

- Parties

- Liabilities

- Present Housing Expenses

- Assets, Purchase Credits, Gifts &

Grants

- Loan Details

- Property

- Declarations

The information entered on the Application page

will flow to the correspondent fields on the other

tabs. For example, if you enter the Sales Price of

property on the Application page, the entered

amount will automatically show on the Collateral

Details page. Conversely, if you update the Sales

Price on the Collateral Details page, the

correspondent value will automatically be updated

on the Application page.

Additionally, we have added the functionality

to pull a credit report directly from the

Application screen for your convenience.

For Help information, select Application.

Note: The final URLA release is planned for the

December release and you will be able to turn it

on anytime between 1/1/2021 (Early Adoption) or

3/1/2021 (Mandatory Regulatory Date). The

Application page will continue to be enhanced

prior to the effective date. We are working to

take all the valuable feedback we’ve received from

you at our Monthly Mortgage Insider’s calls and

make sure all application data is collected in one

place where possible.

- Previously, Declarations and Present Housing

Expenses information was gathered in the Fannie

Mae 1003 Freddie Mac 65 Universal Residential Loan

Application or Credit Application Real Estate

documents. As a part of the October 2020 release,

this information will not be collected on

documents. Instead, the information will be

collected on the Application page.

- WK E-Sign

-

New functionality has been added that allows

for a parallel signing experience when there are

multiple parties that need to sign a package. This

new functionality allows each party to sign and

merge their signatures onto a single PDF if they

have e-consented prior to sending the WK E-Sign

package. It is very important that your financial

institution monitors the consenting of each party

prior to sending to WK E-Sign in order to not

violate ESIGN/UETA rules.

To use the new Parallel Signing feature, you

will need your WK E-Sign Administrator to contact

your WK E-Sign Support Specialist at esignsupport@wolterskuwer.com to verify

your institution's WK E-Sign account is set up for

Parallel Signing. Your WK E-Sign configuration

will need to be set to Smart Consent. Within the

transaction, you will see a new option for

Parallel Signing under Fulfillment Options when

using Interactive Signing. When Parallel

Signing this is selected and a package has

more than one signer, their signatures will be

merged onto a single PDF(s) after both/all parties

have signed.

- When Package Level Consent is set up in your

WK E-Sign configuration, you will notice

Additional Authentication Required is now

always selected and locked down for Electronic

Delivery. You no longer need to remember to select

this option. If your institution is set up for

Smart Consent, Additional Authentication

Required will still be optional.

- Modification

- There were circumstances where on a

Modification, when a collateral was set to

“released”, the system was giving a user not

authorized error. This has now been resolved.

- Financial Analysis

- When Account Number was blank for an Asset,

Liability or Source of Funds on the Financial

Analysis page, NULL displayed when using Internet

Explorer or Edge browsers. This issues has been

resolved.

- Fannie Mae/Freddie Mac

- For Fannie Mae loans when the collateral is

Condo and Freddie Mac loans when the collateral is

PUD, the Property is not located in a

project was changed to Property is located

in a project and will display as selected on

the Add Property view. The change enable

successful submissions to Loan Product Advisor and

Desktop Underwriter.

Changes to Interfaces

- This release does not include changes to

interfaces.

|

| September 2020 |

What's New New Functionality

- The first column of the Projected Payments Table

on the Loan Estimate and Closing Disclosure has

been updated to show the P&I payment as a

single value instead of the min/max range. This

applies to non-construction variable loans where

the Initial Hold Term entered 1) does not

constitute a whole number of years and 2) is

greater than 1 year.

Changes to Interfaces

- This release does not include changes to

interfaces.

|

| August 2020 |

What's New New Functionality

- Wolters Kluwer E-Sign functionality has been enhanced in ComplianceOne and the

Interactive Signing feature has been added to WK

E-Sign. If licensed for this interface, you can

send a package through WK E-Sign via the Print

page within the transaction. To review the new

functionality, select Wolters Kluwer E-Sign (WK E-Sign)

for detailed Help information.

- IMPORTANT: If you are configured for

Package Level Consent within WK E-Sign (ie.

Additional Authentication Required is always

checked and locked when sending a package), you

will need to manually check the Additional

Authentication Required checkbox until a future

release. If you have additional questions on your

WK E-Sign consent status, contact Wolters Kluwer

E-Sign Support at 1-800-529-1582, Option 2.

- Wolters Kluwer now supports the Secured

Overnight Finance Rate (SOFR) index that is an

alternative to the LIBOR index. The index will be

available on the Calculations page in the Index

Name list for variable in-house loans. If the

30-day Average SOFR Index is selected, and

a rate is entered when setting up a variable-rate

policy in Administration, the index and rate will

default when the policy is selected at transaction

time.

Changes to Interfaces

- The August release does not include updates to

interfaces; however, if you are licensed for WK

E-Sign, accessing the interface via the menu is

not longer needed. Enhanced functionality for WK

E-Sign is available now on the Print page within

the transaction. WK E-Sign will remain in the

menu, providing time to learn about the new

functionality and train your staff until it is

removed from the menu in a future release.

|

| July 2020 |

What's New New Functionality

- The Fannie Mae 1003 Freddie Mac 65 Universal

Residential Loan Application will no longer print

section X. Information For Government Monitoring

Purposes. Previously, the section was available

for non-HMDA transactions when neither the

Demographic Information Collected

Separately nor the Government Monitoring

Information Collected Separately was selected

within the Document Data.

Note: ComplianceOne allows collection of

disaggregated demographic data separate from the

application on the Demographic Information

Addendum or the Government Monitoring Information

document. The Demographic Information

Addendum is available in Document Data if:

- HMDA Applies is selected on the Loan

Definition page or Government Monitoring

Information For ECOA (Regulation B) is

Requested is selected on the Document Data

page; and

- Demographic Information Collected

Separately is selected on the Document Data

page.

The Government Monitoring Information is

available in Document Data if:

- HMDA Applies is not selected on the

Loan Definition page; and

- Both Government Monitoring Information For

ECOA (Regulation B) is Requested and

Government Monitoring Information Collected

Separately are selected on Document Data

page.

In addition, an issue that began with the

June release was resolved. In the previous

release, the Fannie Mae 1003 Freddie Mac 65

Universal Residential Loan Application was not

selected for non-HMDA transactions when

Demographic Information Collected

Separately was selected in the Document Data.

This document will now display in the document

list when Demographic Information Collected

Separately is selected.

Changes to Interfaces

- The July release does not include updates to

interfaces.

|

| June 2020 |

What's New New Functionality

- As a continuation of our COVID-19 Emergency offering, we have now added COVID-19

Emergency Suspended Payment Forbearance Plan

Extension, which can extend the original

forbearance plan, as well as the COVID-19

Emergency Payment Deferral Agreement which is

to be used when the loan comes out of

forbearance.

Please note that these

forbearance documents should be used for in-house

mortgages ONLY, and they are not designed to be

used for federally- backed mortgage loans. The

Plan is simply the first step in the process where

you are agreeing to forbear a certain number of

payments. The Extension is to be used to extend

the forbearance, if needed, and the Deferral

Agreement will be used to detail the effect on

payments at the end of the forbearance.

We’ve designed these documents to not

require transaction data to complete. You can

complete data entry in these documents in Document

Data. If you recall your first COVID transaction

where you completed a Forbearance Plan, the data

will be reused where applicable on the two new

documents. To use these new documents,

either recall an existing transaction or start a

new transaction, go to the Closing phase, and

select Post Closing package. Under Transaction

Data, the COVID-19 Emergency Suspended Payment

Forbearance Plan Extension and COVID-19 Emergency

Payment Deferral Agreement options will display.

Select the applicable option and complete the

document. Note: For an empty transaction where

you do not want to complete the other pages,

simply complete the document. Then, take one of

the following approaches:

- Have an Administrator, with rights to

override validation warnings, override each

transaction to remove the Incomplete watermark as

validation will look for collateral and

calculations data.

- Create a template for these COVID-19

transactions and enter fake collateral with a

property address state, possibly a fake seller,

and fake calculations. This template will avoid

the need to override validation warnings.

Remember: The COVID-19 Emergency documents

do not use data from the transaction, so the fake

data will not affect this document.

Changes to Existing Functionality

- Previously, when a liability was added and

linked to a Real Estate Owned property on the

Financial Analysis page, the liability did not

save after a user left the page. The issue has

been resolved as a part of this release.

Changes to Interfaces

- The June release does not include updates to

interfaces.

|

| May 2020 |

What's New

- The May release does not include updates to

What's New with Documents.

- The May release does not include updates to

What's New with Documents.

Changes to Existing Functionality

- The May release does not include updates to

existing functionality.

Changes to Interfaces

- The May release does not include updates to

interfaces.

|

| April 2020 |

What's New Changes to Existing

Functionality

- Select What's New with Docs to review document

changes.

- Based on customer request, we have implemented The COVID-19 Emergency Suspended Payment

Forbearance Plan document within ComplianceOne

Assumptions. The forbearance plan should be used

for in-house mortgages ONLY, and is not designed

to be used for federally-related mortgage loans.

The Plan is simply the first step in the process

where you are agreeing to forbear a certain number

of payments. We are in the process of developing a

separate document to be used to extend the

forbearance, if needed, and a separate agreement

that will be used to detail the effect on payments

at the end of the forbearance (i.e. extending the

maturity date and adding the payments to the end

of the loan). These additional documents will be

available at a later date, knowing that within 3

months, you will need to connect with your

customer and make a plan for the end of the

forbearance.

We’ve designed this document to

not require transaction data to complete and you

can completely fill out this document in Document

Data. To use this new document, you are able to

either recall an existing transaction or start a

new transaction, go to the closing phase, and

select Post Closing package. Under Transaction

Data, the COVID-19 Emergency Suspended Payment

Forbearance Plan option will display. Select this

option and complete the document. Note: For an

empty transaction where you do not want to

complete the other pages, simply complete the

document. Then, take one of the following

approaches:

- Have an Administrator, with rights override

validations, override each transaction to remove

the Incomplete watermark as validation will look

for collateral and calculations data.

- Create a template for these COVID-19

transactions and enter fake collateral with a

property state address, possibly a fake seller,

and fake calculations. This template will avoid

the need to override validation warnings.

Remember: The COVID-19 Emergency Suspended

Payment Forbearance Plan does not use data from

the transaction, so the fake data will not affect

this document.

Changes to Interfaces

- This release does not include changes to

existing functionality.

|

| March 2020 |

What's New Select What's New with Docs to review document

changes. Changes to Existing Functionality

- Previously, the revised version of URLA was available for

transactions created with a template that was new or modified as

of 2/1/2020, that used a Document Policy with the following

option checked: Select the Fannie Mae 1003 Freddie Mac 65

Uniform Residential Loan Application (URLA) . The

current version of the URLA should have been selected. The issue

was fixed on 2/13/20. If you created a new template or modified

a template with that document policy option checked during that

date range and used it for a transaction, you can update your

existing transactions and templates so the current version of

URLA will be available on the Document Data page. Please do the

following:

- Refresh the Document Policy for that existing

transaction on the Loan Definition page.

- Reopen the impacted templates.

Changes to Interfaces

- This release does not include updates to interfaces.

|

| February 2020 |

What's New Select What's New with Docs to review document

changes. Changes to Existing Functionality

- As part of the on-going URLA update project, the assets list on

the Financial Analysis page has been rearranged into two

sections: Assets and Purchase Credits. Lot Equity and

Relocation Funds were added as purchase credit types

and will print in the Assets section of Credit Application Real

Estate and Fannie Mae 1003 Freddie Mac 65 Universal Residential

Loan Application documents until the revised URLA is

supported.

- Previously, if the USDA Technology Fee was added to a Fee

Policy, the fees in that Fee Policy were not pulled into the

transaction. Changes were made so fees included in a Fee Policy

will be included in a transaction when the USDA Technology Fee

has been added to a Fee Policy.

Changes to Interfaces

- Secure Document Exchange (SDX) has been renamed to Wolters

Kluwer E-sign. If you are licensed for Secure Document Exchange

(SDX),"Wolters Kluwer E-sign" will display in areas that

previously displayed Secure Document Exchange (SDX).

|

| January 2020 |

What's New Select What's New with Docs to review document

changes. Changes to Existing Functionality

- As a part of the on-going URLA update project, the Monthly Rent

option has been removed from the Physical Address section on the

Parties page. The Monthly Rent amount will now be based on the

amount entered for the Rent liability entered on the Financial

Analysis page and default to the revised URLA when it is

available in a future release.

- Previously, details entered for an asset type on the Financial

Analysis page did not save unless the tab key was used or

another field was selected on the Financial Analysis page after

entering the details. This behavior was changed so the details

entered for the asset will save if you leave the Financial

Analysis page after entering the data.

Changes to Interfaces

- This release does not include updates to interfaces.

|