View 4b: Loan Origination Page/New or Refinanced Loan at Closing (Part Two)

- LTV (Loan to Value) Ratios

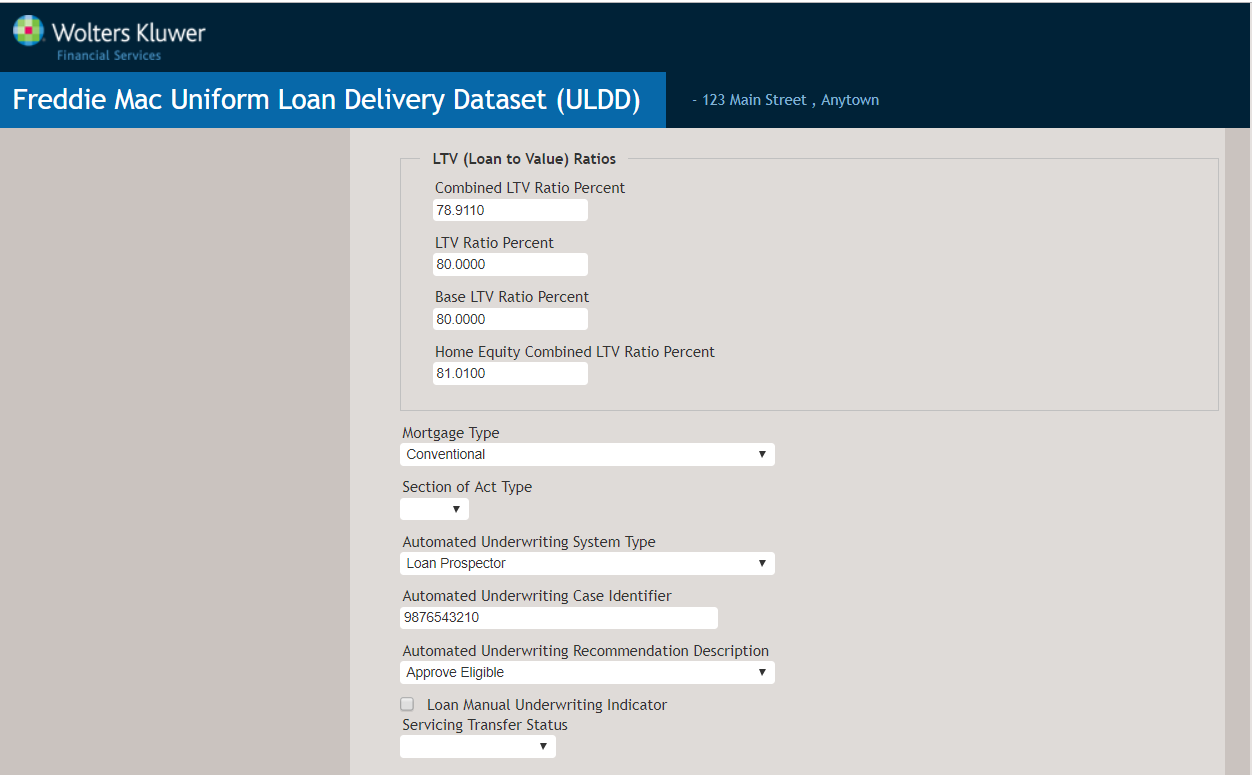

- Combined LTV (CLTV) Ratio [ID 91] (required)

Enter the CLTV Ratio that is the result of dividing the combined unpaid principal balance (UPB) amounts of the first and all subordinate mortgages, excluding undrawn home equity lines of credit amounts, by the value of the subject property. If a first mortgage has no subordinate liens, enter the loan-to-value ratio of the first mortgage.

- LTV Ratio Percent [ID 255] (required)

Enter the LTV Ratio that is the current UPB amount to the appraised value, estimated value, or purchase price of the property.

- Base LTV Ratio Percent [ID 254] (required)

Enter the Base LTV Ratio that is the result of dividing the difference of the original unpaid principal balance (UPB) minus the financed mortgage insurance premium by the value of the subject property.

- Home Equity Combined LTV (HCLTV) Ratio [ID 92] (conditionally

required for loans with a concurrently closing HELOC or an existing

HELOC).

Enter the HCLTV Ratio that is the result of dividing the sum of the unpaid principal balance (UPB) of the first mortgage, the full amount of any home equity line of credit (whether drawn or undrawn), and the balance of any other subordinate financing by the value of the subject property.

- Combined LTV (CLTV) Ratio [ID 91] (required)

- Mortgage Type [ID 317] (required)

Select the type of mortgage being applied for or that has been granted. Options include:

- Conventional

- FHA [limited mortgage support]

- Other: If Other is selected, the 'Public And Indian Housing' option displays.

- USDA Rural Housing [limited mortgage support]

- VA [not supported by mortgage]

- Section of Act Type [ID 198]

This option identifies the section of the National Housing Act that defines underwriting guidelines for VA or FHA loan evaluations. Options include:

- 184

- 203B

- 234C

- 502

- 8

- Automated Underwriting System Type [ID 326/327] (conditionally required

if loan has not been manually underwritten)

Select the type of automated underwriting system used to evaluate the loan. Options include:

- Assetwise

- Capstone

- Clues

- Desktop Underwriter

- ECS

- Loan Prospector

- Other: If Other is selected, options include:

- First Mortgage Credit Score

- Loan Product Advisor

- Strategyware

- Zippy

- Automated Underwriting Case Identifier [ID 322] (required)

Enter the numeric value (Casefile ID) used to identify the unique number for the Loan Prospector/Loan Product Advisor service assigned to the mortgage that is used for tracking subsequent activity related to the mortgage.

- Automated Underwriting Recommendation [ID 325] (conditionally

required)

Select the loan approval recommendation determined by the LP/LPA automated underwriting system. Options include:

- A1 Accept

- A2 Accept

- Accept

- Approve

- Approve Eligible

- C1 Caution

- C2 Caution

- Caution

- Caution Eligible For A Minus

- The Loan was Manually Underwritten [ID 328] (required)

Select if the loan underwriting decision is based on manual underwriting and not the recommendation from an automated underwriting system.

- Servicing Transfer Status (not used)