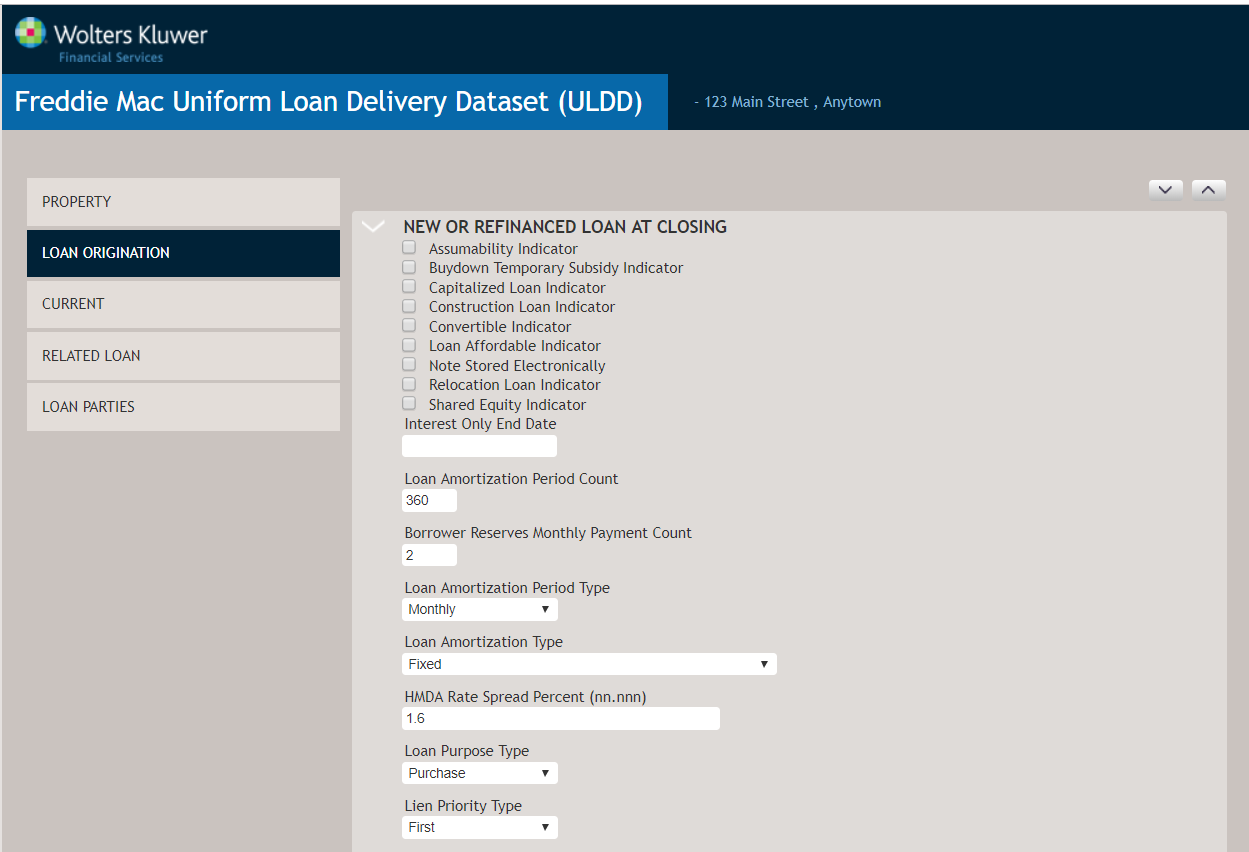

View 4a: Loan Origination Page/New or Refinanced Loan at Closing (Part One)

The loan origination page collects additional at closing time data about the subject loan.

Indicators (required)

The indicators listed below are required information. Select the applicable indicator if the characteristic applies to the loan being delivered.

Assumability Indicator [ID 225]

Select if the loan is assumable by another borrower.

Buydown Temporary Subsidy Indicator [ID 228]

Select if there is a temporary buydown subsidy. A subsidy is money paid by the borrower or third party for the purpose of paying down the interest rate or reducing the monthly payments.

Capitalized Loan Indicator [ID 229]

Select if the loan has been modified or is an Option Adjustable Rate Mortgage (ARM). Capitalized mortgages are those in which accrued interest, taxes, hazard insurance premiums and/or late charges are added to the unpaid principal balance of the loan. Interest capitalization occurs any time interest (accrued and unpaid) and loan fees are added to the outstanding principal balance of a loan.

Construction Loan Indicator [ID 231]

Select if the loan is a construction loan.

Convertible Indicator [ID 232]

Select if the loan has a convertible characteristic.

Affordable Loan Indicator [ID 238]

Select if the loan is a Home Possible Mortgage or identified as an affordable Mortgage in your Seller's negotiated term.

Note Stored Electronically [ID 233]

Select if at the time of delivery, the Note is stored electronically (eNote) rather than by traditional paper documentation.

Relocation Loan Indicator [ID 241]

Select if the loan is part of a corporate relocation program.

Shared Equity [ID 243]

Select if the property has a shared equity mortgage. These mortgages are typically done as part of an affordable lending program with a government agency or nonprofit sharing some of the costs (and ownership), and thereby incurring lower payments or costs to purchase for the homeowner. All loans (first or second) with a shared equity feature are to be identified as shared equity loans, regardless of the form of the investor.

Interest-Only End Date [ID 218] (Not Used)

Enter the number of periods (as defined by the Loan Amortization Period Type) over which the scheduled loan payments of principal and/or interest are calculated to retire the obligation.

Borrower Reserves Monthly Payment Count [ID 287] (required)

Enter the number of loan payments that are available to the borrower from verified financial reserves after closing.

Loan Amortization Period Type [ID 137] (required)

Select the duration of time used to define the period over which the loan is amortized. Selecting Monthly is required.

Loan Amortization Type [ID 138] (required)

Select a classification or description of the loan generally based on the changeability of the rate or payment over time. Options include:

- Adjustable Rate

- Fixed

- Rate Improvement Mortgage: Select 'ate Improvement Mortgage' for Affordable Merit Rate Mortgages.

HMDA Rate Spread Percent (nn.nn) [ID 208] (conditionally required)

Enter the spread (difference) between the annual percentage rate (APR) on the Mortgage and the Average Prime Offer Rate (APOR). Do not enter the APR, APOR, or the Note Rate. The rate spread should be calculated consistent with the methodology provided in HMDA (Regulation C) and the requirements for determining Higher Priced Mortgage Loans (Regulation Z). For mortgages with a rate spread reported under HMDA, a Seller should deliver to Freddie Mac the same rate spread reported under HMDA.

Loan Purpose Type [ID 315]

Select the purpose for which the loan proceeds will be used. Options Include:

- Purchase

- Refinance

Lien Priority Type [ID 313] (conditionally required)

- First

- Second