Section 13. Safeguard Exceptions

Regulation CC lists, in Section 13 [12 CFR 229.13], a number of circumstances in which you can delay the availability of deposits beyond the time limits established in Sections 10 and 12. These are known as the “safeguard exceptions,” and there are six of them. We will first review the circumstances in which the safeguard exceptions apply. Then we will look at the additional time allotted for making the funds available if a safeguard exception applies. Finally, we will look at the notice you must supply the customer if you delay availability because of a safeguard exception.

New Accounts

The first is the exception for new accounts. A new account, for purposes of this exception, is an account that has been open for 30 days or less. However, the account is not considered a new account, even if it has been open 30 days or less, if each customer on the account has had another “established” transaction account with you within 30 days prior to the opening of the new account. An “established” transaction account is one that has been open for at least 30 days. [12 CFR 229.13(a)(2)] Therefore, if a customer is opening an individual account and the initial deposit is a transfer of money from the customer’s “established” transaction account, the new account would not be a new account for purposes of this exception because the customer holds an established transaction account at the time of opening.

Suppose two customers are opening a joint account, and one of them has an established transaction account with you and the other does not and has not within the previous 30 days. In this case, the new account would be a new account for purposes of the exception because not all of the account holders have had an established transaction account with you in the previous 30 calendar days. [Commentary, §229.13(a)-1.b.vi] If a customer has an established savings account but does not have an established transaction account, and has not had an established transaction account in the previous 30 days, any transaction account that customer opens would be a new account for purposes of the exception because the established account must be a transaction account to make the exception not applicable.

Here are the availability rules that apply to new accounts:

- Cash deposits and electronic payment deposits must be made available within the same time frames as required by Section 10. [12 CFR 229.13(a)(1)(i)] See the earlier discussion of Section 10 for details.

- $5,000 [Per Final Rule, $5,525 effective 7/1/20] of deposits of

the following types must be made available as required by

Section 10:

- U.S. Treasury checks

- U.S. Postal Service money orders

- Federal Reserve Bank and Federal Home Loan Bank checks

- Checks drawn by a state or a unit of general local government

- Cashier’s, certified, teller’s, and traveler’s checks

(Notice the inclusion of traveler’s checks here.

Traveler’s checks are not required by any other

section of Regulation CC to be available on the next

business day. This means that a deposit of a

traveler’s check to an established account is not

subject to next-day availability but a deposit of

one to a new account is subject to next-day

availability for the first $5,000 [$5,525 effective

7/1/20]. This curious result was a part of the

statute and so the Board is stuck with it. We have

no explanation for its existence.)

[12 CFR 229.13(a)(1)(ii)]

- The excess over $5,000 [$5,525 effective 7/1/20] of these types of checks need not be made available until the ninth business day after the day of deposit. [12 CFR 229.13(a)(1)(ii)]

- The $200 [$225 effective 7/1/20]] rule of Section 10, which requires next-day availability of $200 [$225 effective 7/1/20] worth of checks other than those already required by Section 10 to be available on the next business day, does not apply to new accounts. Neither does the “on-us” rule of Section 10, which requires next-day availability of checks deposited in a branch of the depositary bank and drawn on the same or another branch of the same bank if both branches are located in the same state or the same check-processing region. [12 CFR 229.13(a)(1)(iii)]

- Section 12, which specifies availability for local and nonlocal checks, does not apply to new accounts, which means the institution can establish any availability time frame it wants for these checks when they are deposited in a new account. [12 CFR 229.13(a)(1)(iii)] (As we pointed out in Part I of this manual in the chapter dealing with your initial funds availability disclosure, you will have to disclose the availability time frame you decide on for these deposits, and you will have to meet the time frame you disclose. But you can choose any time frame you want.)

Large Deposits

The second safeguard exception is for large deposits. A large deposit occurs when a customer deposits in a single banking day more than $5,000 [Per Final Rule, $5,525 effective 7/1/20] in checks. The rule is that Sections 10 and 12 do not apply to the amount deposited in excess of $5,000 [$5,525 effective 7/1/20]. If a customer has more than one account with you, you can aggregate all check deposits to all the accounts in order to see if the large-deposit exception applies even if the customer is not the sole owner on all the accounts. [12 CFR 229.13(b)]

You may apply this exception to local checks normally subject to the Section 12 time limits. You may also apply this exception to “next-day” items, normally subject to next-day availability under Section 10, other than cash and electronic deposits. [Commentary, § 229.13(b)-1]

If a particular deposit of over $5,000 [$5,525 effective 7/1/20] is composed of a combination of next-day and local checks, you can decide which portion of the deposit will be subject to the safeguard exception and which will be made available within the normal maximum time frames. [Commentary, §229.13(b)-1] For example, if the customer deposits a $5,000 next-day check and a $5,000 local check at the same time, you may apply the safeguard exception to either the next-day check or the local check, and make the other available within its normal time frame.

Although you do not have to meet the time frames of Sections 10 and 12 when this exception applies, you are still required to make the funds available within a reasonable period of time after the normal availability time frame. We will discuss that requirement later. That requirement applies to deposits subject to all of the remaining safeguard exceptions as well.

Redeposited Dhecks

The third safeguard exception is for redeposited checks, that is, checks that are being redeposited after having already been deposited once and returned unpaid. The rule here is that the availability time limits do not apply to these checks. [12 CFR 229.13(c)] However, the exception does not apply to checks that have been returned unpaid because an indorsement was missing and the required indorsement has been supplied at the time of the redeposit. The exception also does not apply if the reason for return was that the check was postdated and the check is no longer postdated at the time of the redeposit. [12 CFR 229.13(c)(1) and (2)] In both of these cases, the reason for the return must be stated on the check; if not, you are authorized to apply the exception. [Commentary, §229.13(c)-2]

The availability of the redeposited check is calculated using the date of redeposit as the day of deposit. The redeposit can be by either the customer or the depository institution. [Commentary, §229.13(c)-3]

This safeguard exception can be used to delay the availability of any check, but not the availability of electronic deposits. Also, the exception does apply to the next-day availability of the first $200 [$225 effective 7/1/20] of a check deposit on a single day. [12 CFR 229.13(c)] (See discussion of Section 10 above.) This means that if you made $200 [$225 effective 7/1/20] of a check available for withdrawal under the next-day availability rule and the check is returned unpaid, you may charge back the $200 [$225 effective 7/1/20] and need not make it available again if the check is redeposited. [Commentary, §229.13(c)-3]

Repeated Overdrafts

The fourth safeguard exception applies when a customer has been repeatedly overdrawing his or her accounts. The Regulation defines two circumstances in which you can consider a customer a “repeat overdrawer.” The first is when on six or more banking days during the past six months, the customer’s account balance is negative or would have been negative if checks presented against the account or other charges had been paid. The second is when on two or more banking days in the past six months, the customer’s account balance is negative in the amount of $5,000 [Per Final Rule, $5,525 effective 7/1/20] or more or would have been negative by that amount if checks presented against the account or other charges had been paid. [12 CFR 229.13(d)(1) and (2)]

If a customer has more than one account with you, you can total the number of these instances in the past six months for all the customer’s accounts to decide whether the exception can be applied. The instances can be related to separate checks or charges, or they could be related to only one overdraft. [Commentary, §229.13(d)-1] For example, the exception would apply to a customer who in the past six months wrote six separate checks that overdrew the account and would also apply to a customer who wrote only one check that overdrew the account but who allowed the account balance to remain negative for six banking days. (However, a single check that is returned unpaid can only count as one instance of overdraft.) [Commentary, §229.13(d)-1]

If your customer is a “repeat overdrawer” under either test, then this safeguard exception applies for a period of six months after the particular overdraft that triggered the exception. [12 CFR 229.13(d)] In other words, you may delay the availability of any next-day items (other than cash or electronic deposits) or local checks that the customer deposits within six months of writing the overdraft that caused the customer to be a “frequent overdrawer.” The length of the delay for particular checks is determined by the rules we will review after going over the rest of the safeguard exceptions.

Reasonable Cause to Doubt Collectibility of Item

The fifth safeguard exception is when you have reasonable cause to doubt the collectibility of the deposited check. [12 CFR 229.13(e)] According to the Regulation, “Reasonable cause to believe a check is uncollectible requires the existence of facts that would cause a well-grounded belief in the mind of a reasonable person. Such belief shall not be based on the fact that the check is of a particular class or is deposited by a particular class of persons.” [12 CFR 229.13(e)] Examples of when this exception might apply are when you receive notice from the paying bank that a check is being returned, or when you receive notice from a paying bank prior to presentment that the check is not collectible because the drawer’s account has insufficient funds or because the drawer has stopped payment on the check. Checks deposited over six months after the date on the check (stale-dated checks) are subject to this exception, as are postdated checks. A reasonable belief on your part that the customer is engaged in kiting activity would also entitle you to apply this exception. [Commentary, §229.13(e)2.a.-d.]

These are just a few examples cited by the Commentary to the Regulation of circumstances where this exception could be applied. Others undoubtedly exist, and it is ultimately up to you to apply the standard quoted above to a particular set of facts to decide whether the exception applies.

The reference to not applying the exception to particular classes of checks or persons means, for example, that you could not decide to apply the exception to all checks drawn on rural institutions or to all checks deposited by persons of a certain race or national origin. [Commentary, §229.13(4)-4] The Regulation seems to be saying that you should employ this safeguard exception only on a check-by-check basis and not have a policy that applies the exception invariably to certain types of checks or depositors.

You can apply this exception to all next-day items (other than cash and electronic deposits), to local checks, and to nonlocal checks. [12 CFR 229.13(d)]

Emergency Conditions

- An interruption of communications or computer or other equipment facilities;

- A suspension of payments by another bank;

- A war; or

- An emergency condition beyond the control of the depository bank if the depository bank exercises such diligence as the circumstances require.

[12 CFR 229.13(f)(1) - (4)]

When this exception applies, you can delay the availability of next-day items (other than cash and electronic deposits), local checks, and nonlocal checks. [12 CFR 229.13(f)] You can only apply the exception to checks that are affected by the emergency conditions. [Commentary, §229.13(f)-1]

Length of Delay

Once you’ve decided that you can apply a safeguard exception to a particular deposit, you need to decide how long you can delay the availability of the deposit. We have already mentioned the length of delays applicable under the new account exception. Under that exception, the excess over $5,000 [$5,525 effective 7/1/20] of next-day availability items deposited in a single banking day (other than cash and electronic payments) need not be made available until the ninth business day after the day of deposit. Local checks normally subject to Section 12 are subject to whatever availability time frame you disclose in your initial disclosure. [12 CFR 229.13(a)]

When one of the other safeguard exceptions applies, you can delay availability beyond the normal required time frames by a “reasonable” period of time. [12 CFR 229.13(h)(1)] The Regulation deems five business days to be reasonable for local checks. [12 CFR 229.13(h)(4)] (Next-day items are treated as if they were local checks. [12 CFR 229.13(h)(2)] ) Longer periods of time may, in some cases, be reasonable but the burden is on you to show that the longer period of time is reasonable in a particular situation. This means that should the issue of the length of your delay ever be litigated, the burden is on you to prove the reasonableness of a delay that is longer than the five-business-day delay deemed reasonable by the Regulation. [12 CFR 229.13(h)(4)]

Delaying availability beyond the normal required time frames means beyond the second business day for local checks. [12 CFR 229.13(h)(1)] For example, if a safeguard exception applies to a local check, you can extend availability for five business days (deemed to be a reasonable period) beyond the second business day after the day of deposit (the normal availability time frame for local checks); i.e., until the seventh business day after the day of deposit.

When a safeguard exception is used to delay the availability of a next-day item, then the delay is for a reasonable period of time beyond what the required availability would be if the checks were treated as local checks under Section 12, rather than the Section 10 time frames. [12 CFR 229.13(h)(2)] This is not true, however, for “on us” checks, which are checks deposited in a branch of the depository bank and drawn on the same or another branch of the bank if both branches are located in a single state or check processing region. If you apply a safeguard exception to an “on us” check, you may delay availability only one business day, until the second business day after the banking day of deposit. [12 CFR 229.13(h)(4)]

If the deposit is made at a nonproprietary ATM, then the delay is a reasonable period beyond the fifth business day. [12 CFR 229.12(f)] And, finally, if the emergency exception is invoked, the delay can be extended a reasonable period after (1) the emergency is over or (2) the normal required time frame has expired, whichever is later. [12 CFR 229.13(h)(3)]

You should know that there is an ambiguity concerning these “length-of-delay” rules that affects institutions taking advantage of the $400 [$450 effective 7/1/20] cash withdrawal rule. The issue is whether you add the delay period to the normal availability time frames or to the normal availability time frames as extended by the $400 [$450 effective 7/1/20] cash withdrawal rule. Recall that the $400 [$450 effective 7/1/20] cash withdrawal rule allows you to delay the availability of a deposit an extra day for purposes of withdrawals by cash, except for $400 [$450 effective 7/1/20] of the deposit, which must be available for cash withdrawal by 5 P.M. of the last day of the normal availability time frame. [12 CFR 229.12(d)] To take advantage of the $400 [$450 effective 7/1/20] cash withdrawal rule, you must describe it in your initial disclosure form. [Commentary, §229.16(b)-7] (See our earlier section in this chapter dealing with the $400 [$450 effective 7/1/20] cash withdrawal rule.)

So if you apply a safeguard exception to a local check, do you add the five-day delay period to the second business day after the day of deposit (the normal availability time frame) or to the third business day after the day of deposit (the normal availability time frame as extended by the $400 [$450 effective 7/1/20] cash withdrawal rule)? We have always interpreted the Regulation and Commentary as requiring the period be added to the normal availability time frame without the extra day extension. In March of 1997, however, the Board amended the Regulation and Commentary. While none of the amendments dealt with this issue, some language in the Supplementary Information (which is introductory explanatory text accompanying the amendments) suggested the period be added to the extended availability time frame.

Since the language in the Supplementary Information is itself ambiguous and lacks the force of law the Regulation and Commentary carry, we are reluctant to encourage anyone to rely on it. If you are interested in reading the language itself, however, you can find it in the Federal Register for March 24, 1997, at page 13801 (federalregister.gov/documents/1997/03/04, page 7 of the downloaded issue).

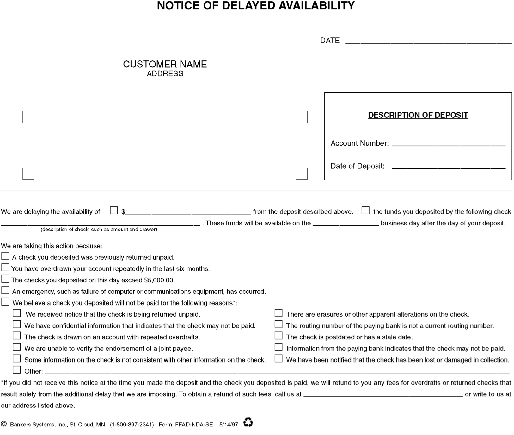

Notice of Delay to Customer

- A number or code, which need not exceed four digits, that identifies the customer's account;

- The date of the deposit;

- The amount of the deposit that is being delayed;

- The reason the exception was invoked (including the reason for doubting the collectibility of the check, if that is the exception invoked, unless that reason is confidential, and then you may indicate that you have confidential information that indicates that the check might not be paid) [Commentary, §229.13(e)-2.d.]; and

- The time period within which the funds will be available for withdrawal.

[12 CFR 229.13(g)(1)(i)]

Form FFAD-NDA-SE is the notice form to give to the customer when you are delaying the availability of a deposit in reliance on a safeguard exception.

Although the notice must be in writing, it need not be on paper. You can satisfy the written notice requirement by sending an electronic notice that displays the text and is in a form that the customer may keep, if the customer agrees to such means of notice. Information is in a form that the customer may keep if, for example, it can be downloaded or printed. [Commentary, §229.13(g)-1]

The Regulation provides model forms for the safeguard exception notice. These are model forms C-12 and C-13. C-12 is the general notice form and C-13 is the notice form for the “reasonable cause” exception and contains a list of circumstances constituting “reasonable cause.” Most institutions combine these two model forms into a single form, and this is certainly a practical and permissible thing to do. The form shown above is an example.

You must give this notice to the depositor at the time the deposit is made. [12 CFR 229.13(g)(1)(ii)] There are four exceptions to this timing requirement, however.

First, if the deposit is not made in person or if the facts that cause you to invoke the exception do not become known to you until after the deposit is made, you can mail or deliver the notice to the customer no later than the business day after the day you learn the facts or the day of the deposit, whichever is later. [12 CFR 229.13(g)(1)(ii)]

[If the safeguard exception you are invoking is the “reasonable cause to doubt collectibility” exception and you do not supply the notice until after the deposit is made, then you are subject to a restriction in charging overdraft and returned check fees. You cannot impose an overdraft fee (including a fee for use of an overdraft line of credit) or a returned check fee if (1) the only reason the account was overdrawn or the check(s) returned was the delay of availability of the check and (2) the check is paid. However, you can charge these fees under these circumstances if you include on your notice form a statement that the customer may be entitled to a refund of the overdraft or returned check fees if the check subject to the exception is paid, and you also include an explanation as to how to obtain the refund. You must also, of course, make the refund when required. [12 CFR 229.13(e)(2)] Remember, the restriction on charging those fees only applies when the “reasonable cause” safeguard exception is invoked and the notice is given after the time of deposit.]

Under the second exception to the timing rule, you need not give a notice each time you invoke an exception if: (1) the account is a nonconsumer account (one that is not used for personal, family, or household purposes); (2) the safeguard exception you are invoking is either the large deposit exception or the redeposited check exception; (3) you will invoke the exception for most deposits to the account to which the exception applies (e.g., you will invoke the large deposit exception most times a customer makes a check deposit totaling over $5,000 [$5,525 effective 7/1/20]); and (4) you give a special one-time notice at or before the first time you would otherwise give the safeguard exception notice. The special notice must state the reason(s) the safeguard exception may be invoked and the time period in which deposits subject to the exception will generally be available for withdrawal. [12 CFR 229.13(g)(2)] Regulation CC provides model Form C-14 for this notice.

The third exception to the timing rule also allows you to avoid giving a notice each time you invoke a safeguard exception. If the repeated overdrafts safeguard exception applies to a depositor, you may give a single, one-time notice to the depositor that will apply to the entire six-month period the repeated overdrafts exception applies. The one-time notice must include: (1) the account number of the customer, (2) the fact that the availability of funds deposited in the customer’s account will be delayed because the repeated overdrafts exception will be invoked, (3) the time period in which deposits subject to the exception will generally be available for withdrawal, and (4) the time period during which the exception will apply. You can use this one-time notice option on both consumer and nonconsumer accounts. However, you must be planning on applying the exception to most check deposits made to the account during the period the exception applies. [12 CFR 229.13(g)(3)] Regulation CC provides model Form C-15 for this notice.

- …a depositary bank may learn of a weather emergency or a power outage that affects the paying bank’s operations. Under these circumstances, it likely would be reasonable for the depositary bank to provide an emergency conditions exception notice in the same manner and within the same time as required for other exception notices. On the other hand, if a depositary bank experiences a weather or power outage emergency that affects its own operations, it may be reasonable for the depositary bank to provide a general notice to all depositors via postings at branches and ATMs, or through newspaper, television, or radio notices. [Commentary, §229.13(g)-4.a.]