Additional Disclosure Requirements

- Posted statements of your funds availability policy,

- Notices posted (or available) at your ATMs,

- Disclosures to be given when your funds availability policy changes,

- Notices on preprinted deposit slips, and

- Disclosures of your funds availability policy given on request.

We could have included our discussion of these disclosure requirements in our chapter in Part I dealing with account opening responsibilities under Regulation CC. However, we wanted to limit that chapter strictly to the things that you must do when a customer opens an account. These other disclosure requirements are more general and ongoing in nature and are not related specifically to an individual account opening.

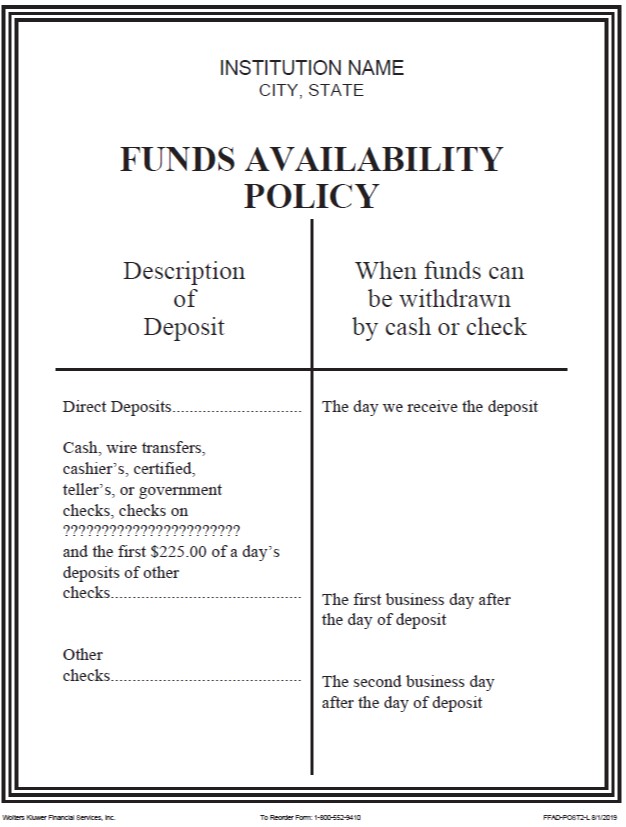

Posted Statement of Your Policy

The first of these additional disclosure requirements is the posted statement of your funds availability policy. You are required to post, in a conspicuous place, a notice that “sets forth the time periods applicable to the availability of funds deposited in a consumer account.” [12 CFR 229.18(b)] You only have to post this notice at locations where your employees receive deposits to consumer accounts. [12 CFR 229.18(b)] (“Consumer account” is defined as an account used primarily for personal, family, or household purposes. [12 CFR 229.2(n)] ) Therefore, you do not need to post it at other unstaffed locations where you receive deposits, such as night depositories or locations where you only receive deposits to nonconsumer accounts or do not receive deposits at all.

Unfortunately, the Regulation and Commentary are not very clear as to how detailed this posted notice must be. You could read the requirement that you set forth “the time periods applicable to the availability of funds” as requiring a statement of all the possible time periods that might apply, including those that arise when a safeguard exception or a case-by-case exception is invoked. If so, an explanation of those exceptions might also be appropriate.

However, it is likely that something less is required. The Regulation supplies two model forms for this posting, one for institutions with policies that make all deposits available on the first business day after the day of deposit and one for institutions that delay availability to the extent permitted by the Regulation. Judging from these model forms, you don’t need to include very much on a poster. The next-day availability model poster reads simply: “FUNDS AVAILABILITY POLICY: Our general policy is to allow you to withdraw funds deposited in your account on the [number] business day after the day we receive your deposit. In some cases, we may delay your ability to withdraw funds beyond the [number] business day. Then, the funds will generally be available by the fifth business day after the day of deposit.” [12 CFR 229, Appendix C, form C-18] The other model poster, for those who restrict availability to the maximum time limits, is simply a chart with the types of deposits listed on the left side and the availability time frames on the right. [12 CFR 229, Appendix C, form C-17] Neither poster mentions the safeguard exceptions, and so it is probably safe to leave them out of your poster.

You only need to post this notice in a place where depositors are likely to see it before making a deposit; you do not need to have one posted at each teller window. [Commentary, §229.18(b)-1] You also do not have to have one posted at your drive-up window. [Commentary, §229.18(b)-1]

Financial institutions must post brief descriptions of their funds availability policies.

Notices at ATMs

- AVAILABILITY OF DEPOSITS: Funds from deposits may not be available for immediate withdrawal. Please refer to your institution’s rules governing funds availability for details.

This notice must be posted or provided at any ATM at which customers can make deposits to their accounts with you. [12 CFR 229.18(c)(1)] The responsibility for making sure the notice is provided is yours, whether the ATM is proprietary or nonproprietary, but you can arrange for the owner or operator of a nonproprietary ATM to take care of the notice and indemnify you for any liability you incur because of its absence. [Commentary, §229.18(c)‑1]

This notice must be either posted or provided. [12 CFR 229.18(c)(1)] That means you can post it in a conspicuous place, have it appear on the ATM’s screen, or provide it on deposit envelopes at the ATM. The notice must be available to the customer before the deposit is made, which means that putting the notice on a deposit receipt or on an ATM screen presented to the customer after the deposit is made is insufficient. [Commentary, §229.18(c)‑2]

- NOTICE: Deposits at this ATM between [day] and [day] will not be considered received until [day]. The availability of funds from the deposit may be delayed as a result.

Remember, this disclosure requirement only applies to off-premise ATMs that you operate. You don’t need to worry about on-premise ATMs and ATMs that you do not operate, regardless of how frequently deposits are collected from them.

Statement on Preprinted Deposit Slips

- Deposits may not be available for immediate withdrawal.

The notice must appear on the front of the deposit slip.[Commentary, §229.18(a)-1]

This requirement only applies to “preprinted” deposit slips, which the Commentary to Regulation CC defines as those preprinted with the customer’s account number and name and that you supply in response to the customer’s order. [Commentary, §229.18(a)-1] The notice does not have to appear on deposit slips that do not have the customer’s name and account number preprinted, such as counter deposit slips. [Commentary, §229.18(a)-1]

You are also not responsible for deposit slips that the customer receives from someone other than you. [Commentary, §229.18(a)-1] You can accept those slips even if they do not contain the notice and you will not be in violation of Regulation CC.

Notice of Change in Policy

The fourth additional disclosure requirement is the disclosure you must send to customers if you change your funds availability policy. The disclosure must state what the change is and must be sent to holders of “consumer” accounts at least 30 days prior to the effective date of the change, unless the change expedites the availability of funds, in which case, the notice can be sent not later than 30 days after the effective date of the change. [12 CFR 229.18(e)] Again, you only have to send the notice to holders of “consumer” accounts, which are accounts used primarily for personal, family or household purposes. (To be safe, you should send the notice to any accounts that you know are consumer accounts and any that might be consumer accounts. Also, you should consider whether you have an obligation for some reason other than Regulation CC to send a notice to non-consumer accounts. For instance, your account agreement might provide that you will give notice of change. Or, you may be concerned that it would be unfair or deceptive if you do not give notice.)

You can either send notice of only the changes in your policy or you can send a disclosure of your entire new funds availability policy. If you send your entire policy, you must point out the provisions that are new, either by enclosing a letter or insert, or highlighting the new provisions in the disclosure. [Commentary, §229.18(e)-1]

An added element of this fourth disclosure requirement affects institutions whose funds availability disclosures contain a list of either proprietary or nonproprietary ATMs. As we pointed out in Part I of this manual, if your policy distinguishes the availability of deposits made at nonproprietary ATMs from those made at proprietary ATMs, your initial disclosure must instruct the customer on how to tell the two types of ATMs apart. One way of doing this is to include a list of the locations of either your proprietary ATMs or your nonproprietary ones. Institutions that have included such a list with their initial disclosure must send out an updated list once per year if there have been any changes to the list that they provided to the customers. [Commentary, §229.18(e)-3]

Policy Disclosure Provided on Request

The fifth additional disclosure requirement is that you provide a copy of your initial policy disclosure to anyone upon his or her written or oral request. [12 CFR 229.18(d)] You must send the notice within a reasonable period of time after you receive the request. This rule applies whether or not the person making the request is a customer of yours. [Commentary, §229.18(d)-1]