Case-by-Case Exceptions

If your funds availability policy makes any category of deposits available for withdrawal more quickly than required under the Regulation, you can delay the availability of those deposits on a case-by-case basis beyond your normal time frame and up to the time frame required for availability by the Regulation. [12 CFR 229.16(c)(1)] For example, if your policy is to make local checks available on the first business day after the day of deposit, you can, on a case-by-case basis, delay the availability of local checks until the second business day. You can do this without changing your general policy or your initial disclosure form.

- The account number of the customer;

- The date of the deposit;

- The amount of the deposit that is being delayed; and

- The day the funds will be available for withdrawal.

[12 CFR 229.16(c)(2)(i)]

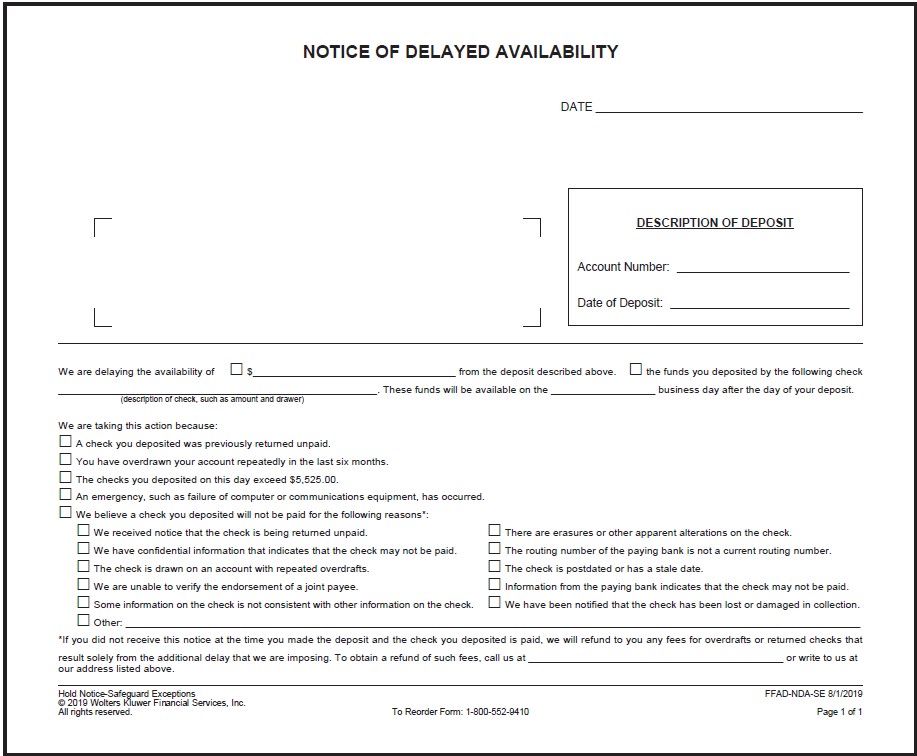

Form FFAD-NDA-CBC is the notice form to give the customer when you are delaying availability of a deposit in reliance on your authority to do so on a case-by-case basis.

Although the notice must be in writing, it need not be on paper. You can satisfy the written disclosure requirement by sending an electronic disclosure that displays the text and is in a form that the customer may keep, if the customer agrees to such means of disclosure. Information is in a form that the customer may keep if, for example, it can be downloaded or printed. [Commentary, §229.15(a)-1]

You must give the notice to the depositor at the time the deposit is made unless the deposit is not made in person or your decision to make the case-by-case delay is not made until after the deposit. In either of those cases, the notice must be mailed or delivered to the depositor no later than the first business day after the banking day of deposit. [12 CFR 229.16(c)(2)(ii)]

If you give the notice sometime after the deposit, you are subject to a restriction on charging overdraft and returned check fees similar to the restriction that applies under the “reasonable cause” safeguard exception. You cannot impose an overdraft fee (including a fee for use of an overdraft line of credit) or a returned check fee if (1) the only reason the account was overdrawn or the check(s) returned was the delay of availability of the check, and (2) the check is paid. However, you can charge these fees if you include on your notice form a statement that the customer may be entitled to a refund of the overdraft or returned check fees if the check subject to the exception is paid, and you also include an explanation as to how to obtain the refund. You must also, of course, make the refund when required. [12 CFR 229.16(c)(3)]

The Regulation supplies model Form C-16 for making the notice of case-by-case exceptions.

Again, the delay that you can impose under the case-by-case authority extends only up to the normal availability time frames required under the Regulation. [12 CFR 229.16(c)(1)] If you want to extend the delay beyond that point, circumstances justifying a safeguard exception must be present and you must give the notice required for safeguard exceptions.

Since a case-by-case delay can last only up to the appropriate maximum availability time frame, it seems logical that any case-by-case delay you impose would be subject to the $200 [$225 effective 7/1/20] next-day availability rule. Recall that you must make the first $200 [$225 effective 7/1/20] of non-next-day check deposits in any one banking day available for withdrawal not later than the business day after the banking day of deposit. [12 CFR 229.10(c)(1)(vii) See “The first $200…“ in “Section 10, next day availability items” above.] The case-by-case delay authority simply allows you to delay up to the required time frames a deposit your normal policy would make available more quickly. Since the $200 [$225 effective 7/1/20] next-day availability rule is a required time frame, it would not be superceded by a case-by-case delay. Language in the model forms suggests this is correct. [12 CFR 229, Appendix C, Form C-3]