| December 2018 |

What's New Take Advantage of a Complimentary

Quick Start to What’s New? Get up and running

quickly with our overview of the ComplianceOne mortgage changes so you

know what to expect in our next release. Attend a complimentary

“What’s New” webinar, hosted by our experienced software trainers. For

available dates, times, and to register, sign-in on our Support website, and

navigate to your ComplianceOne mortgage product page.Note: Beginning

in January 2019, What's New Instructor-let Webinars will be replaced

with on-demand, recorded tutorials that will be available 24/7. We

will continue to provides links each month to the recorded tutorial in

this section in What's New Help.Click to review What's New with the

Documents Click to review the Document

List New Functionality

- The Bureau of Consumer Financial Protection issued an

interpretive and procedure rule on August 31, 2018 to

implement and clarify the Economic Growth, Regulatory

Relief, and Consumer Protection Act which amends HMDA and

creates a partial exemption applicable to transactions

with an Action Taken Date on or after 1/1/2018.

Organizations that are partially exempt have the option of

reporting exempt data.

On the Loan Definition page,

Partially Exempt per S. 2155 has been added

to the HMDA section and is available when 2018

HMDA Applies is selected. When setting up your

Loan Definition Policy in Administration, you can

indicate if Partially Exempt per S. 2155

defaults selected or not, and if you want to

Allow User to Edit Field in Transaction.

- On existing transactions where a Loan Definition

policy is used, Partially Exempt per S.

2155 defaults unselected and is editable until

the Loan Definition policy is updated in

Administration and Loan Definition Policy

is refreshed on the Loan Definition page.

- On existing transactions where a Loan

Definition policy is not used, Partially Exempt

per S. 2155 defaults unselected.

If you are licensed for the HMDA Wiz interface,

any existing transaction with an Action Taken

Date on or after 1/1/2018 will need to be

updated if you are a partially exempt lender. Those

existing transactions can be updated using the Grid

view on the Edit page within HMDA Wiz. If you

are not licensed for the HMDA Wiz interface, you

will have to open each transaction and select

Partially Exempt per S. 2155 on the Loan

Definition page and then recreate your pipe

delimited file(s). The following questions

have been added to the HMDA Reporting section in

How do I identify a transaction as partially exempt per Senate Bill 2155 for HMDA Reporting?, If I select Partially Exempt per S. 2155 on the

Loan Definition page, how will that impact my

transaction?, and My organization is regulated by the FDIC or OCC;

how do I continue to report the Reasons for Denial

on my partially exempt

transactions?

Updates to Existing Functionality What's New for Interfaces New

Functionality

- We have reordered the information on the HMDA Preview LAR

report to provide a more consistent experience across our

products and to allow for easier review of the

information. For those users who use ComplianceOne Lending

and/or ARTA Lending, the order of the information in the

reports will be in the same for all products. For those

users that are licensed for the HMDA Wiz interface, the

order of the information in the report will follow the

order of data on the Edit page within HMDA Wiz.

-

If you are a licensed HMDA user and try to use

Geocoding, Rate Spread and Insert/Update services

with the wrong credentials, a validation message

displays directing you to verify your credentials in

Interface Manager. To validate your credentials,

visit the HMDA Wiz website, test your credentials,

and make changes if needed in Interface Manager.

- If there is an Appraisal Identifier entered on the

Collateral Details page, it will be transferred to the

Property Information section of the Loan Product Advisor

underwriting system. The Appraisal Identifier field is

available within ComplianceOne Mortgage / Assumptions if

type of Mortgage is Fannie Mae, Freddie Mac, or FHA.

- If the user selects the specific appraisal Form Number used

to report the property valuation that can be entered on

the Uniform Underwriting and Transmittal document, the

Form Number will be sent to Loan Product Advisor. This is

required if there is an Appraisal Identifier available in

the transaction.

If there is a Valuation Method

being selected on the Collateral Details page, this

information will transfer to Loan Product Advisor.

This is a required information to be reported to the

third-party underwriting system if the property

valuation has been done on the property and there is

an Appraisal Identifier available. The following

question has been added to the Automated Underwriting

section in Help: What property valuation information should be submitted to Loan Product Advisor?

- Product Description has been added to the Loan

Product Advisor interface view. This is the lender's

unique identifier of a mortgage product or program

associated with the loan, allowing the lender to

distinguish between different loan offerings.

- If there is a property seller in the transaction who is an

individual or sole proprietor, the seller's

First-/Middle/Last-/Suffix Names will be now transferred

to Loan Product Advisor.

Updates to Existing Functionality

- What's New for Interfaces

- New Functionality

-

- ComplianceOne® Insiders

- Note: The Insiders meetings have changed from

two times per month to one time per month. We will

adjust as the need arises.

Here's your chance to

be on the “inside” of the ComplianceOne mortgage

development discussions. Be heard in this monthly

group (3rd Thursday each month), during a one-hour

roundtable discussion to gather your input and

feedback on functionality that is being updated or

added to ComplianceOne mortgage. We look

forward to engaging with you! Register

Here using the password:

Mtg2018

|

| November 2018 |

- What's New

- Take Advantage of a Complimentary Quick Start to

What’s New?

- Get up and running quickly with our overview of the

ComplianceOne mortgage changes so you know what to

expect in our new release. Attend a complimentary

“What’s New” webinar, hosted by our experienced

software trainers. Select What's New in November to

access the training webinar.Note: What's New

webinars are no longer available at http://training.wolterskluwerfs.com/. You

can now access the webinars from links in What's New

Help or by selecting Support

Website and logging in. Navigate to the

ComplianceOne mortgage product page, select View

All Product Training and select

ComplianceOne Mortgage What's New webinars.

- Click to review What's New with the

Documents

- Click to review the Document

List

- New Functionality

- An individual contact type of Loan

Processor is now collected in Administration

on the Contacts page and a default Loan

Processor is collected on the Organizations

page. Within a transaction and a template, Loan

Processor has been added to the General

Information section on the Loan Definition page.

After your administrator enters the loan processor

contact(s), the information entered in

Administration for the Loan Processor

selected on the Loan Definition page will print in

the Contact Name, Contact Title, Contact Phone

Number, and ext. fields on the Uniform

Underwriting and Transmittal Summary for new and

existing transactions.

- On the Loan Definition page, an option must be

selected for the Construction Note Type to

create a construction loan and calculate

accurately. If an option is not selected and

Construction is selected for the Integrated

Disclosure Purpose, the following message

displays on the Loan Definition page: "Select an

option under Construction Note Type to create a

construction loan" and the following message

displays on the Print page as a warning:

"Construction Note Type should be set up for

transactions with Integrated Disclosure Purpose

equal to Construction."

For existing

transactions where the Integrated Disclosure

Purpose Type of Construction was chosen and

the Rate Type is variable, the

Product field, where variable rate program

is described, is showing the incorrect value for

the initial rate hold term on the documents listed

below:

- Adjustable Rate Mortgage Program

- Lock Agreement-MN

- Lock in Agreement-MT

- Loan Estimate

- Closing Disclosure

- Rate Lock Agreement

- Fannie Mae 1003 Freddie Mac 65 Uniform

Residential Loan Application

- Fannie Mae 1003 Freddie Mac 65 URLA Uniform

Residential Loan Application‐CA

- Fannie Mae 1003 Freddie Mac 65 URLA Uniform

Residential Loan Application‐DC

- Fannie Mae 1003 Freddie Mac 65 URLA Uniform

Residential Loan Application‐OH

- Mortgage Loan Commitment

You will want to visit the Loan Definition

page to select the appropriate Construction

Note Type, calculate, and recreate documents

if necessary.

- The credit bureaus' address, phone number,

internet address, and credit score range numbers

will now populate the Risk Based Pricing Notice,

Risk Based Pricing Notice - Credit Score, and

Notice of Action Taken after completing a credit

pull in ComplianceOne Lending and transferring the

loan to ComplianceOne mortgage. A re-issue of the

credit report or a credit bureau refresh in

Financial Analysis will no longer need to be

completed.

- Updates to Existing Functionality

- Previously, if the Combine Assets/Liabilities

option for co-applicants on the Parties Page was

cleared and a user navigated away from the page

and returned, the option displayed selected. This

issue was resolved and the option will remain

cleared.

- Purchase, non-construction transactions with

the Application Received Date on or after

10/1/2018 and where the Loan Amount is

equal to Sales Price should be recalculated

to show the accurate amount of Down Payment/Funds

from Borrower and Funds for Borrower on the Loan

Estimate and Closing Disclosure documents. To

publish the correct value in the Application Phase

of the transaction, select Calculate on the

Calculation Details page. As of 10/1/18, this

value was calculated incorrectly by removing the

Closing Costs Financed (if present) before

comparing the Total Existing Debt Being

Satisfied and the Loan Amount.

- In the Loan Terms section on the Loan Estimate

and Closing Disclosure, an issue has been resolved

where 'Yes' was printing for Can this amount

increase after closing? for the Interest Rate row.

This occurred when the Application Received

Date was on or after 10/1/2018, Construction

Only was selected for Construction Note

Type on the Loan Definition page, Variable was

selected for Rate Type on the Calculations

page, and after calculating the Rate Type

was changed to Fixed. For existing transactions,

review, calculate, and recreate the Closing

Disclosure if necessary.

-

- What's New for Interfaces

- New Functionality

- The Location ID entered in Administration for

your organization will now be sent to the Loan

File Setup section in the Loan Product Advisor

underwriting service.

- The explanations selected for any Yes answer

to a declaration on lines a through i on the

Uniform Residential Loan Application Continuation

Page or Credit Application Real Estate Supplement

are now transferred to Desktop Underwriter

(DU).

- Updates to Existing Functionality

- Previously, the dependent ages entered on the

Uniform Residential Loan Application document

(section III) were not transferred to Desktop

Underwriter. This has been resolved and if

dependent ages are entered, they will be

transferred to Desktop Underwriter.

- Loan demographic data including ethnicity,

race, sex, and basis of collection for the data

will populate mortgage when performing an import

from Mortgagebot.

- ComplianceOne® Insiders

- Note: The Insiders meetings have changed from

two times per month to one time per month. We will

adjust as the need arises.

Here's your chance to

be on the “inside” of the ComplianceOne mortgage

development discussions. Be heard in this monthly

group (3rd Thursday each month), during a one-hour

roundtable discussion to gather your input and

feedback on functionality that is being updated or

added to ComplianceOne mortgage.

- These are complimentary, open to all

ComplianceOne mortgage users, and require

pre-registration.

- The agenda for each session will be posted one

week prior on the registration website allowing

you to plan which roundtable you can impact the

most!

We look forward to engaging with you!

Register

here using the password:

Mtg2018

|

| October 2018 |

- What's New

-

This release marks the launch of the Vanceo™

Mortgage. Congratulations! If you are reading

this, you and your financial institution have made

a great decision, and will now be able to leverage

Vanceo™ Mortgage to drive internal controls and

efficiencies in your daily financial processes.

For more information, refer to the Vanceo Dashboard page in Help.

- Take Advantage of a Complimentary Quick Start to

What’s New?

- Get up and running quickly with our overview of the

ComplianceOne mortgage changes so you know what to

expect in our new release. Attend a complimentary

“What’s New” webinar, hosted by our experienced

software trainers. Select What's New in October to

access the training webinar.Note: What's New

webinars are no longer available at http://training.wolterskluwerfs.com/. You

can now access the webinars from links in What's New

Help or by selecting Support

Website and logging in. Navigate to the

ComplianceOne mortgage product page, select View

All Product Training and select

ComplianceOne Mortgage What's New webinars.

- Click to review What's New with the

Documents

- Click to review the Document

List

- New Functionality

- On the Loan Definition page in the HMDA

section, Business or Commercial Purpose is

used to report the loan as a business or

commercial purpose to HMDA and displays unselected

by default. The Business or Commercial

Purpose selection is strictly for HMDA

reporting purposes, and the transaction will be

treated as a consumer purpose loan for all other

purposes.

- On the Calculations page in the Monthly

Housing Expenses section, All Other Monthly

Payments is now automatically calculated. The

calculated amount is a sum of all liabilities

entered on the Financial Analysis page except for

Mortgage, Leasehold Payment, Ground Rent and Other

Housing Expense. The calculated amount can be

changed if needed. The All Other Monthly

Payments value is used by the Uniform

Underwriting and Transmittal Summary

document.

- On the Calculations page in the

Origination/Disposition section, 4 = Collateral

will now default selected for Reasons for

Denial when 'Location or condition of

collateral (use only in Massachusetts)' is

selected for Reason Type in the Action

Reason section of Document Data for the Notice Of

Action Taken document. You will need to manually

select 4 = Collateral for Reasons for Denial

on any existing transaction that has 'Location

or condition of collateral (use only in

Massachusetts)' selected for Reason Type.

- An issue has been resolved where if more than

one instance of Assessment or County Property Tax

had been entered for Proration Type on the

Closing Disclosure page and both instances were

assigned to the same Integrated Disclosure

Subsection, then only the first instance

printed to the Closing Disclosure. For example, on

the Closing Disclosure page, you enter

Proration Item of Assessment and

Integrated Disclosure Subsection of

Adjustments for Items Unpaid by Seller and an

amount of $200. You also enter another

Proration Item of Assessment and

Integrated Disclosure Subsection of

Adjustments for Items Unpaid by Seller and an

amount of $100. In this scenario, the second

Assessment for $100 would not print to the Closing

Disclosure. This issue has been resolved for

transactions with an Application Received Date

on or after 10/1/2018, so review, calculate

and recreate documents if necessary. For

transactions with an Application Received

Date prior to 10/1/2018 (in which the closing

occurs after 10/1/2018), you will need to continue

to aggregate the amounts and enter one proration

on the Closing Disclosure page.

- Updates to Existing Functionality

This

release does not include updates to existing

functionality.

- What's New for Interfaces

- New Functionality

- Previously, when lenders used a credit service

outside of ComplianceOne, a validation error

displayed for Credit Identifier that

prevented submissions to the GSE Automated

Underwriting Service (i.e. Fannie Mae DU or

Freddie Mac LP). The validation error was removed

and submissions to the GSE Automated Underwriting

Service will now be successful.

- Manual Geo Codes entered on the Collateral

page and Manual Rate Spreads entered on the

Calculations page now import and override

automated Geo Codes and automated Rate Spreads in

HMDA Wiz and CRA Wiz.

- Updates to Existing Functionality

This

release does not include updates to existing

functionality.

- ComplianceOne® Insiders

- Note: The Insiders meetings have changed from two

times per month to one time per month. We will

adjust as the need arises.

Here's your chance to

be on the “inside” of the ComplianceOne mortgage

development discussions. Be heard in this monthly

group (3rd Thursday each month), during a one-hour

roundtable discussion to gather your input and

feedback on functionality that is being updated or

added to ComplianceOne mortgage.

- These are complimentary, open to all

ComplianceOne mortgage users, and require

pre-registration.

- The agenda for each session will be posted one

week prior on the registration website allowing

you to plan which roundtable you can impact the

most!

We look forward to engaging with you!

Register

here using the password:

Mtg2018

|

| September 2018 |

- What's New for ComplianceOne® mortgage

- Take Advantage of a Complimentary Quick Start to

What’s New?

-

Get up and running quickly with our overview of

the ComplianceOne mortgage changes so you know

what to expect in our next release. Attend a

complimentary “What’s New” webinar, hosted by our

experienced software trainers. Select What's New in

September to access the training

webinar.

- Click to review What's New with the

Documents

- Click to review the Document

List

- New Functionality

- Several improvements were made to the

following areas:

- Headers

- Template Maintenance

- Party Management

- HMDA Processing

Although the changes are small, they

impact several areas. All the current

functionality is still available but the look and

feel of the main landing page header has been

updated to provide easier viewing and navigation.

The information below provides details about the

changes. Transaction Header The

transaction header has been updated.

- The home icon has been replaced with

that brings you back to a

main page. that brings you back to a

main page.

- Selecting your name brings you to your User

Profile.

- Selecting Help opens up Help

information.

- Selecting Logout ends your

session.

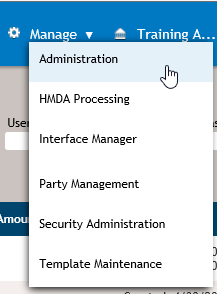

Manage To access

Administration, HMDA Processing, Interface

Manager, Party Management, Security

Administration, or Template Maintenance management

functions that were previously in the

ComplianceOne menu, select Manage in the

header and an option. The selected function will

open in a new browser tab. The lending browser tab

will remain open so you can easily return and

continue work after you finish with the newly

opened tab. To close a management function such as

Administration, close the browser tab.

Old

New

HMDA Processing, Party Management and

Template Maintenance Headers The look

and feel of the HMDA Processing, Party Management,

and Template Maintenance headers were updated to

match the new transaction header. However, HMDA

Processing, Party Management, or Template

Maintenance display instead of ComplianceOne.

- When a transaction is recalled from HMDA

Processing, the transaction header shows you came

from HDMA Processing. Selecting the brings you back to the HMDA

Processing landing page.

- When a party is recalled from Party

Management, the transaction header shows you came

from Parties. Selecting brings you back to the

Parties landing page.

- When a template is recalled from Templates,

the transaction header shows you came from

Templates. Selecting brings you back to the

Templates landing page.

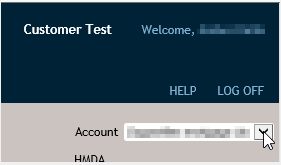

Accessing

Accounts Account was moved from

inside a page to the header. To access a different

account if you are licensed for more than one

account, select the account in the header.

Old

New

- In the May release, we added validation

messaging to the Loan Definition and Print pages

alerting you that transactions with an Application

Received Date of 10/1/2018 or later were not yet

supported. Since then, we have been making changes

each release to implement the TILA RESPA

Integrated Disclosures (TRID) amendments. We have

completed all of the changes and the validation

messaging has been removed from the Loan

Definition and Print pages. A summary of the

changes and when they were released is included

below:

- May Release: What’s New with

Documents

- June Release: Calculating Cash to Close

Table-Adjustments and Other Credits

- June Release: Calculating Cash to Close

Table – Seller Credits; June release

- June Release: Help only changes

- Closing Disclosure page; Gift Funds

- Calculations and Closing Disclosure page;

Seller Credits

- July Release: Escrow Account table

- Escrowed Property Costs over Year

- Estimated total amount over year 1 for your

escrowed property costs

- Escrow Payment

- July and September Release:

Improvements Value

- August Release: Inspection and Handling

Fees

- August Release: Calculating Cash to

Close Table-Closing Costs Financed

- August Release: Calculating Cash to

Close Table-Down payment/Funds from Borrower and

Funds for Borrower

- September Release: Loan Terms-Principal

and Interest row (See below)

- September Release: Adjustable Payment

(AP) Table (See below)

- September Release: Closing Costs

Expiration (See below)

- The TRID amendments, applicable to

transactions with an Application Received

Date on or after 10/1/2018, allow a creditor,

issuing a revised Loan Estimate after the consumer

has indicated an intent to proceed within the time

specified by the creditor, to leave the date and

time the estimate closing costs are to expire

blank. On the Calculations page in the application

phase, we have removed the required symbol from

the Date, Time, and Time Zone

within the Closing Costs Expiration section. When

the Closing Costs Expiration Date,

Time, and Time Zone are blank and the

Application Received Date is on or after

10/1/2018, the language on page one of the Loan

Estimate is as follows: '...closing costs expire

on.'

In addition, we have also hidden the

Closing Costs Expiration section of the

Calculations page within template maintenance due

to a customer request.

- The TRID amendments, applicable to

transactions with an Application Received

Date on or after 10/1/2018, allow a user to

include the estimated value of improvements to be

made on a property when disclosing an Appraised

Value or an Estimated Value for a construction

loan without a seller. On the Collateral Details

page in the Application phase, the user can enter

the amount in Improvements Value. The

entered value will be added to the

Estimated/Appraisal Value on the Loan Estimate and

Closing Disclosure.

- For transactions with an Application

Received Date on or after 10/1/2018 that have

multiple property taxes or homeowner’s insurance,

some of which are escrowed, 'Some' will print in

the 'In Escrow' section on the Closing Disclosure.

Changes were made so this transaction type can be

submitted to Uniform Closing Dataset (UCD) without

error.

- The TRID amendments, applicable to

transactions with an Application Received

Date on or after 10/1/2018, added comment

7(iv) to Appendix D of Regulation Z. Specifically

the disclosure requirements for the ‘Can this

amount increase after closing’ of the Principal

and Interest row within the Loan Terms section and

the Adjustable Payment (AP) table have been

updated. Both of these sections on the Loan

Estimate and Closing Disclosure have been updated

for transactions where Construction Note Type

is Construction Only or Construction and

Permanent Note.

The following question has been

added to the Calculations section in Help: How are the interest-only, payment amounts

typically calculated for multiple advance,

construction loans? The following

questions have been added to the Document Data

section in Help: Within the Loan Terms section, how is the ‘Can this amount increase after closing’ column of Principal and Interest row completed on the Loan Estimate and Closing Disclosure for construction transactions with an Application Received Date on or after 10/1/2018? How are the ‘First Change/Amount’, ‘Subsequent Changes’, and ‘Maximum Payment’ rows of the Adjustable Payment (AP) Table completed on the Loan Estimate and Closing Disclosure for construction transactions with an Application Received Date on or after 10/1/2018?

- For transactions where Construction Note

Type is Construction Only or Construction and

Permanent Note, we have addressed an issue related

to the calculation of Closing Cost Financed

and have made some improvements in relation to the

data entry of construction costs and the initial

advance amount.

- When the Application Received Date is

on or after 10/1/2018, Improvements Value

has been relabeled as Construction Costs

within Collateral Details. The amount entered is

the cost to complete the construction or

improvements to the property. The following

questions have been added to the Collateral

section in Help:

- When Application Received Date is on or

after 10/1/2018 and Seller Information is

Unknown is selected, Use Seller Disclosures

on Non-Seller Transaction is selected, or a

seller has been added in Collateral Details, the

Closing Costs Financed (Paid from your Loan

Amount) on the Closing Disclosure is determined by

subtracting the Sales Price, liabilities on

the Financial Analysis page where Payoff is

selected, and Construction Costs from the

Loan Amount. Previously in construction

transactions where a seller had been added, the

Construction Costs were not being

considered in this calculation.

- The Initial Advance Amount is now

collected on the Calculations page in the closing

phase. Previously, the Initial Advance

Amount was entered on the Consumer Note. When

an amount is entered for Initial Advance

Amount, the product will automatically create

an Amount Paid to Third Party disbursement on the

Disbursements page and will also automatically

create an Adjustment on the Closing Disclosure

page.

For existing transactions, the Initial

Advance Amount previously entered in Document

Data will be retained and will appear on the

Calculations page. Because the product will

automatically create a disbursement and an

adjustment with this release, you will want to

visit the Disbursements page and Closing

Disclosure page, if applicable, to remove the

manually entered disbursement and adjustment if

you had created them prior to this release.

The following question have been added to

the Disbursements section in Help: The following question has been added to

the Closing Disclosure section in Help:

- The amount of undisbursed loan proceeds

available for construction, also known as

Construction Holdback, is determined by the

product based on the Construction Costs and

Initial Advance Amount. The product

subtracts the Initial Advance Amount on the

Calculations page from the sum of Construction

Costs for each collateral, if more than one

piece of collateral exists. The amount remaining

is the Construction Holdback resulting in an

automatically created Amount Paid to Third Party

disbursement on the Disbursements page and

automatically created Adjustment on the Closing

Disclosure page.

For existing transactions where

you have previously entered a disbursement and/or

an adjustment for the Construction Holdback, you

will want to visit the Disbursements page and/or

Closing Disclosure page to remove it since the

product will have automatically created a

disbursement and adjustment with this

release. The following question has been

added to the Disbursements section in Help:

-

The following question has been added to the

Closing Disclosure section in Help:

-

On construction only loans, the initial

interest rate is correctly being rounded to three

decimal places. Prior to this release, the

interest rate was rounded to the nearest two

decimal places. For existing transactions, review,

calculate, and recreate the documents to see the

rounding update.

- Updates to Existing Functionality

This

release does not include updates to existing

functionality.

- What's New for Interfaces

- New Functionality

This release does no

include new functionality.

- Updates to Existing Functionality

This

release does not include updates to existing

functionality.

- ComplianceOne® Insiders

- Note: The Insiders meetings have changed from two

times per month to one time per month. We will

adjust as the need arises.

Here's your chance to

be on the “inside” of the ComplianceOne mortgage

development discussions. Be heard in this monthly

group (3rd Thursday each month), during a one-hour

roundtable discussion to gather your input and

feedback on functionality that is being updated or

added to ComplianceOne mortgage.

- These are complimentary, open to all

ComplianceOne mortgage users, and require

pre-registration.

- The agenda for each session will be posted one

week prior on the registration website allowing

you to plan which roundtable you can impact the

most!

We look forward to engaging with you!

Register

here using the password:

Mtg2018

|

| August 2018 |

- What's New for ComplianceOne® mortgage

- Take Advantage of a Complimentary Quick Start to

What’s New?

-

Get up and running quickly with our overview of

the ComplianceOne mortgage changes so you know

what to expect in our next release. Attend a

complimentary “What’s New” webinar, hosted by our

experienced software trainers. Select What's New in

August to access the training webinar.

- Click to review What's New with the

Documents

- Click to review the Document

List

- New Functionality

- On the Collateral Details page,

Construction Method is now available for

all transactions that are not HMDA reportable. For

users licensed for Uniform Loan Delivery Dataset

(ULDD), the selection made for Construction

Method will export to the ULDD interface.

- For transactions with an Application

Received Date on or after 10/1/2018,

Closing Costs Financed (Paid from your Loan

Amount) for the seller version of Cash To Close

table is calculated by subtracting the total

amount of payments to third parties not otherwise

disclosed in the Loan Costs and Other Costs from

the Loan Amount. TRID amendments effective on

10/1/2018 have provided clarifications on what

third parties payments should be taken into

consideration in Closing Costs Financed

calculation and include the following:

- The sale price of property for purchase

transactions.

- The estimated value of improvements to be made

on property for construction transactions.

- The payoffs of secured or unsecured debt.

- For transactions with an Application

Received Date on or after 10/1/2018, the

calculation logic of Down Payment/Funds from

Borrower and Funds for Borrower has

changed. If the transaction is non-construction

purchase, we will subtract the Loan Amount from

the total amount of all existing debt being

satisfied in the transaction. If the transaction

is construction purchase, non-purchase, or if the

Loan Amount exceeds the Sale Price, we will

subtract the Loan Amount (excluding Closing Costs

Financed (Paid from your Loan Amount)) from the

total amount of all existing debt being satisfied

in the transaction. Examples of existing debt

being satisfied include: Sale Price of Property,

Adjustments, and any other charges that may be

disclosed on Line K.04 of Closing Disclosure.

If

the amount calculated is greater than zero, then

this amount will be disclosed as Down

Payment/Funds from Borrower in the Cash To Close

table. If the amount is less than zero, then this

amount will be disclosed as Funds for Borrower.

On the Calculations page, we have added the

Inspection and Handling Fees table within the

Post-Closing Fees section that is available when

Construction Note Type is Construction Only

or Construction and Permanent Note and the

Application Received Date is on or after

10/1/2018. The TRID amendments require inspection

and handling fees collected after closing to be

disclosed on the Loan Estimate Addendum and

Closing Disclosure-Addendum. Although, the

Application Received Date is not visible

within template maintenance, the Inspection and

Handling Fees section is available when

Construction Note Type is Construction Only

or Construction and Permanent Note to allow you to

set up your templates prior to the 10/1/2018

effective date. Inspection and Handling

fees are finance charges and should be included in

the calculations for the In 5 Years total and

Total of Payments figures on the Loan Estimate and

Closing Disclosure. As a result, the Total

for the Inspection and Handling fees will impact

the following figures:

- APR within Calculation Results and in the APR

in the Loan Calculations table on the Loan

Estimate and Closing Disclosure

- In 5 Years total in the Loan Calculations

table on the Loan Estimate

- Total of Payments within the

Calculation Results and in Total of Payments total

in the Loan Calculations table on Closing

Disclosure

- APR Fees within Calculation Results

- Total Charges Affecting the APR within

Calculation Results

- Finance Charge within Calculation

Results

- Amount Financed within Calculation

Results

Lastly, Inspection and Handling Fees are

also included in the federal points and fees test

required under 1026.32 and will be included in

that testing when using the Wiz Sentinel

interface. The following questions have been

added to the Fees section in Help:When disclosing inspection and handling

fees that are paid after closing, does each

individual fee need to be disclosed or is the

total of all inspection and handling fees required

to be disclosed? Do inspection and handling

fees that are collected after closing affect any

of the Loan Calculation values on the Loan

Estimate and Closing Disclosure?

- Updates to Existing Functionality

- On the Collateral Details page, the selection

made for the Manufactured Home Land Property

Interest, will now match the selection for the

Manufactured Home Land Property Interest on the

HMDA Preview LAR report or the pipe delimited text

file. Previously, '5 not applicable' defaulted to

the HMDA Preview LAR report or the pipe delimited

text file.

- 8888 is used for the Credit Score on the HMDA

Preview Report and in the HMDA submission request

for the applicant or co-applicant when the

following conditions apply:

- Credit Score Used in Interface is not

selected on the Financial Analysis page for any

credit bureau response for the applicant or

co-applicant.

- On the Calculations page, the Underwriting

Action Taken is one of the following:

- 1 - Originated

- 2 - Application Approved but not Accepted

- 3 - Application Denied

- 7 - Preapproval Request Denied

- 8 - Preapproval Request Approved but not

Accepted,

- What's New for Interfaces

-

New Features

New Credit Provider

Wolters Kluwer has partnered with SettlementOne

to offer mutual customers access to

SettlementOne’s services. After configuration, the

SettlementOne Credit Service allows users to

submit minimal information about an applicant to

SettlementOne Credit Service to receive a

comprehensive credit report. Users are able to

select from single, dual, or tri-merge credit

reports, along with establishing joint credit

pulls for multiple borrowers. After the user has

finished pulling credit, all transaction and

credit report critical data is returned to

ComplianceOne mortgage.

Customers who are interested in the new credit

service provided by SettlementOne should contact

their Wolters Kluwer sales representative.

Updates to Existing Functionality

-

This release does not include updates to existing

interface functionality.

- ComplianceOne® Insiders

-

Here's your chance to be on the “inside” of the

ComplianceOne mortgage development discussions. Be

heard in this twice a month group (2nd and 3rd

Thursdays each month), during a one-hour

roundtable discussion to gather your input and

feedback on functionality that is being updated or

added to ComplianceOne mortgage.

- These are complimentary, open to all

ComplianceOne mortgage users, and require

pre-registration.

- The agenda for each session will be posted one

week prior on the registration website allowing

you to plan which roundtable you can impact the

most!

We look forward to engaging with you!

Register

here using the password: Mtg2018

|

| July 2018 |

- What's New for ComplianceOne® mortgage

- Take Advantage of a Complimentary Quick Start to

What’s New?

-

Get up and running quickly with our overview of

the ComplianceOne mortgage changes so you know

what to expect in our next release. Attend a

complimentary “What’s New” webinar, hosted by our

experienced software trainers. For available

dates, times, and to register or sign in, select

this link: http://training.wolterskluwerfs.com/.

- Click to review What's New with the

Documents

- Click to review the Document

List

- New Functionality

- With this release you will likely have already

realized we adopted the latest Wolters Kluwer

brand standards for the login and logout pages. In

addition, we’ve redesigned and improved the

usability of our Help. You can now search across

all help topics/pages, print help pages, and

provide feedback inside the help tool. The

familiar pages from the previous version of Help

are now laid out in a tile format on the main page

for easy navigation. Selecting the Wolters Kluwer

logo will bring you back to the main landing page

of Help.

- Select the Question button next to the Search

box for tips on searching.

- Select the Helpful? button on the right to

provide a quick comment about Help

information.

- Select the Feedback button to provide detailed

comments about Help and access Support

information.

- Select the Print button to print the current

page.

- For transactions with an Application

Received Date on or after 10/1/2018, the

Escrowed Property Costs over Year 1 amount within

the Escrow Account section on the Closing

Disclosure can be based on the payments made into

the escrow account during the first year starting

from the First Payment Date when

Calculate escrowed property costs over year 1

using the first payment date is selected for

the applicable Calculations Policy within

Administration. The following question has been

added to the Document Data>Document Specific

section in Help: Within the Escrow Account section on the Closing Disclosure, how is the Escrowed Property Costs over Year 1 determined?

- For transactions with an Application

Received Date on or after 10/1/2018, the

'Escrowed Property Costs over Year 1' amount and

'Escrow Payment' amount in the Escrow Account

table on page 4 will now include mortgage

insurance (PMI, Mortgage Insurance or USDA

Mortgage Insurance) when entered on the

Calculations page.

- On the Closing Disclosure for transactions

with an Application Received Date on or

after 10/1/2018, the description of ‘See attached

page for additional information’ will print in the

Escrow Account table for ‘Estimated total amount

over year 1 for your escrowed property costs’

and/or ‘Estimated total amount over year 1 for

your non-escrowed property costs’ fields when

there is not enough space. In addition, the

detailed description prints on the Closing

Disclosure in the Addendum within the Loan

Disclosures section. Lastly, the description will

include a reference to 'mortgage insurance' when

PMI, Mortgage Insurance, or USDA Mortgage

Insurance is entered on the Calculations

page.

- The TRID amendments that are applicable to

transactions with an Application Received

Date of 10/1/2018 or after have updated the

commentary to §1026.38(j)(2)(vi) to provide

clarification on the disclosure of gift funds on

the Closing Disclosure. No changes were made to

the product. The following question has been added

to the Closing Disclosure section in Help:When are Gift Funds required to be disclosed in the Other Credits section of the Summaries of Transactions section of the Closing Disclosure?

- The TRID amendments that are applicable to

transactions with an Application Received

Date of 10/1/2018 or after have updated the

commentary to §1026.37(h)(1)(vi) to provide

clarification on the disclosure of specific seller

credits on the Loan Estimate. No changes were made

to the product. The following question has been

updated on the Calculations>Loan Estimate and

Closing Disclosure section in Help: How are Seller Credits disclosed on the Loan

Estimate?

- On the Calculations page, changes were made to

improve usability. A new section for Post-Closing

Fees has been added and includes the following:

- Returned Payment Fee that was

previously on the Loan Definition page.

- Late Charges that were previously

included in the Fees section on the Calculations

page.

- On the Document Data page for construction

loans, the Collateral is the Construction

Property check box was removed. Collateral

is the Construction Property was renamed to

Construction Property and relocated on the

Collateral Details page.

-

On the Collateral Details page if

Construction Property is selected,

Improvements Value displays to comply with

TRID amendments effective 10.1.2018 (Comment

37(a)(7)-1). If Improvements Value is

selected, the estimated value of improvements to

be made on the property can be entered for a

construction loan without a seller. In the next

release, the estimated value of improvements will

added and print to the Estimated/Appraisal Value

disclosed on the Loan Estimate and Closing

Disclosure for a construction loan without a

seller.

- Updates to Existing Functionality

- On the Collateral Details page, a ‘Sorry, this

page is currently unavailable’ message displayed

after selecting a party to edit. This issue has

been corrected and any party on the Collateral

Details page can be viewed and edited if a user is

not a read-only user.

- On the Calculations page/Underwriting

Information section/Origination/Disposition, the

Override Reasons for Denial was changed to

Edit Reasons for Denial. If you select

Edit Reasons for Denial, the reasons

selected on the Notice of Action Taken document

will remain defaulted to Origination/Disposition

and can be edited.

- What's New for Interfaces

-

New Features

This release does not include new interface

features.

Updates to Existing Functionality

-

This release does not include update to existing

interface functionality.

- ComplianceOne® Insiders

-

Note: The session for Thursday, July 19 has been

cancelled. We look forward to our next discussion

with you on Thursday, August 9.

Here's your chance to be on the “inside” of the

ComplianceOne mortgage development discussions. Be

heard in this twice a month group (2nd and 3rd

Thursdays each month), during a one-hour

roundtable discussion to gather your input and

feedback on functionality that is being updated or

added to ComplianceOne mortgage.

- These are complimentary, open to all

ComplianceOne mortgage users, and require

pre-registration.

- The agenda for each session will be posted one

week prior on the registration website allowing

you to plan which roundtable you can impact the

most!

We look forward to engaging with you!

Register

Here using the password: Mtg2018.

|

| June 2018 |

- What's New for ComplianceOne® mortgage

- Take Advantage of a Complimentary Quick Start to

What’s New?

-

Get up and running quickly with our overview of

the ComplianceOne mortgage changes so you know

what to expect in our next release. Attend a

complimentary “What’s New” webinar, hosted by our

experienced software trainers. For available

dates, times, and to register, sign-in on our

Support

website, and navigate to your ComplianceOne

mortgage product page.

- Click to review What's New with the

Documents

- Click to review the Document

List

- New Functionality

- Updates to Existing Functionality

- We have removed the option of Principal

Reduction from the Closing Adjustment Item list on

the Closing Disclosure page since it was

inadvertently added in the March release. The

first option in the list, Borough Property Tax,

will default selected for any existing

transactions where you had previously selected

Principal Reduction. It is recommended that you

review the Closing Disclosure page and recreate

documents if necessary.

- What's New for Interfaces

-

New Features

This release does not include new interface

features.

Updates to Existing Functionality

-

This release does not include update to existing

interface functionality.

- ComplianceOne® Insiders

-

Here's your chance to be on the “inside” of the

ComplianceOne mortgage development discussions. Be

heard in this twice a month group (2nd and 3rd

Thursdays each month), during a one-hour

roundtable discussion to gather your input and

feedback on functionality that is being updated or

added to ComplianceOne mortgage.

- These are complimentary, open to all

ComplianceOne mortgage users, and require

pre-registration.

- The agenda for each session will be posted one

week prior on the registration website allowing

you to plan which roundtable you can impact the

most!

We look forward to engaging with you!

Register

here using the password: Mtg2018.

|

| May 2018 |

- What's New for ComplianceOne® mortgage

- Take Advantage of a Complimentary Quick Start to

What’s New?

-

Get up and running quickly with our overview of

the ComplianceOne mortgage changes so you know

what to expect in our next release. Attend a

complimentary “What’s New” webinar, hosted by our

experienced software trainers. For available dates

and times, and to register, sign-in on our Support

website, and navigate to your ComplianceOne

mortgage product page.

- Click to review What's New with the

Documents

- Click to review the Document

List

- New Functionality

- On the Parties Details page, changes were made

to improve usability. Data collection items were

added to the Parties Details page and removed from

the Financial Analysis page as described below.

- The Employment Information section was renamed

to Employment and Income and redesigned.

- Overtime, Bonus, and

Commission were added to the new Employment

and Income page.

- Amount was added and includes the total

of Base Income, Overtime,

Bonus, and Commission included for

an employment.

- Overtime, Bonus, and

Commission were removed from the Financial

Analysis page where this information was collected

previously.

- The Other Income section was added so users

can add other income information directly on the

Parties Details page. In this section,

Dividends/Interest, Net Rental Income, Alimony,

Child Support, Maintenance, Social Security,

Subject Property Positive Cash Flow, Support

Pension, and Other can be selected in the Select

Income Source drop-down list and an amount can be

entered.

- If Other is selected, a custom description and

an amount can be entered.

- Other income sources can be added by selecting

Add and entering a name and amount.

- Support Pension and Social Security are new

income types that have been added to the Select

Income Source drop-down list.

- On the Loan Definition and Print pages,

changes were made to accommodate the final rule

amending the federal mortgage disclosure

requirements under the Truth in Lending Act

(Regulation Z), otherwise known as TRID, that took

effect on October 10, 2017 with a mandatory

compliance date for applications taken on or after

October 1, 2018. We are in the process of updating

the product pages, calculations, and documents to

comply with the new rules. As a result, validation

warnings have been added to Application

Received Date on the Loan Definition page and

the Print page when the Application Received

Date is 10/1/2018 or later, and the system

date is prior to 10/1/2018. This will allow you to

review the new functionality as we make changes in

the upcoming releases which will be communicated

here and in the What's New with the Documents.

(Link to be inserted). After we have completed all

the changes, the validation warnings will be

removed from the Loan Definition page and Print

page.

- On the Calculations page in the Ratios

section, changes were made to improve

usability.

- Include all parties income was added.

This option replaces Additional Parties

Income that was removed from the Financial

Analysis page. If selected, the total income from

all borrowers and cosigners will be included in

the Home to Income (HTI) and Debt to Income (DTI)

calculations.

- Exclude the borrower income and report ‘not

applicable’ for HMDA was added and will

display when 2018 HMDA Rule Applies is

selected on the Loan Definition page. HMDA

reportable income will be excluded and Not

Applicable will be reported to HMDA when

Exclude the borrower income and report ‘not

applicable’ for HMDA is selected. Exclude

the borrower income and report ‘not applicable’

for HMDA was removed from the Financial

Analysis page where it appeared previously.

- On the HMDA page, the name of the reviewer and

the date of the review will display after

Reviewed is selected by a user. A user must

be assigned the HMDA Reviewer permission in

Security Administration before they can select

Reviewed.

- Updates to Existing Functionality

- What's New for Interfaces

-

New Features

Updates to Existing Functionality

- ComplianceOne® Insiders

-

Here's your chance to be on the “inside” of the

ComplianceOne mortgage development discussions. Be

heard in this twice a month group (2nd and 3rd

Thursdays each month), during a one-hour

roundtable discussion to gather your input and

feedback on functionality that is being updated or

added to ComplianceOne mortgage.

- These are complimentary, open to all

ComplianceOne mortgage users, and require

pre-registration.

- The agenda for each session will be posted one

week prior on the registration website allowing

you to plan which roundtable you can impact the

most!

We look forward to engaging with you!

Register

here using the password: Mtg2018.

|

| April 2018 |

- What's New for ComplianceOne® mortgage

- Take Advantage of a Complimentary Quick Start to

What’s New?

-

Get up and running quickly with our overview of

the ComplianceOne mortgage changes so you know

what to expect in our next release. Attend a

complimentary “What’s New” webinar, hosted by our

experienced software trainers. For available dates

and times, and to register, sign-in on our Support

website, and navigate to your ComplianceOne

mortgage product page.

- Click to review What's New with the

Documents

- Click to review the Document

List

- New Functionality

- On the Financial Analysis page, liabilities

that have been closed or paid will now be excluded

from the liabilities that are pulled from a credit

bureau when Exclude zero balance liabilities

that are Paid or Closed is selected in Account

Basics in Administration.

- On the Employer Information page, a Calculate

button has been added to calculate the Years

Employed and Months Employed. The

values for the current employer are based on the

From start date and the system date. The

To end date will not display for a current

employer. The values for the previous employer are

based on the From start date and the

To end date.

- On the Parties Details page, Verification

of Employment and Verbal Verification of

Employment have been added for individual and

sole proprietors who are borrowers and cosigners.

Selecting Verification of Employment will

add the Request for the Verification of Employment

(FNMA 1005) to the document list. Selecting

Verbal Verification of Employment will add

the Verbal Verification of Employment to the

document list and display Employee Badge ID

for entering an ID. Previously, Verification

Requested and Verbal Verification of

Employment Requested were available on the

Document Data page to generate the Request for

Verification of Employment and Verbal Verification

of Employment documents. Previously, Employee

Badge ID was collected in Document Data for

the Request for Verification of Employment.

- The HMDA Reviewer permission has been added to

the mortgage Loan Originator role in Security

Administration. The new permission will default

unchecked. This permission allows a user to select

the Reviewed check box on the HMDA page.

Review your mortgage Loan Originator and custom

roles to activate the permission for your users if

applicable.

- Updates to Existing Functionality

- The Introductory Rate Period (In Months) now

prints in the Loan Information section on the

Preview LAR Record where nothing was printing

previously. When Rate Type is Variable, the

Initial Rate Hold Term from the

Calculations page will print. When Rate

Type is Fixed, NA will print along with Not

applicable in the description.

- Previously, when entering a non-numeric value

for the Year, Length, or

Width on the Collateral page for Mobile

Home (Personal Property/Residence) collateral and

exporting to an interface, an error displayed.

Now, the Year, Length, or

Width will be sent as blank. If numeric

digits are entered, the values will be sent.

- An issue has been resolved where the Cash to

Close amount in the Calculating Cash to Close

table and Summaries of Transaction table, when

applicable, was not summed correctly when the

transaction included a Generalized Lender Credit

and Refund exceeded tolerance amount was

selected on the Calculations page. We have also

addressed an issue where the Specific Lender

Credits amount displayed on the Calculations

page in the closing phase was not including any

fees that were added at closing where Paid

By was Lender. For existing transactions,

review, calculate, and recreate documents if

necessary.

- What's New for Interfaces

-

New Features

This release does not include new features.

Updates to Existing Functionality

-

This release does not include updates to existing

functionality.

- ComplianceOne® Insiders

-

Here's your chance to be on the “inside” of the

ComplianceOne mortgage development discussions. Be

heard in this twice a month group (2nd and 3rd

Thursdays each month), during a one-hour

roundtable discussion to gather your input and

feedback on functionality that is being updated or

added to ComplianceOne mortgage.

- These are complimentary, open to all

ComplianceOne mortgage users, and require

pre-registration.

- The agenda for each session will be posted one

week prior on the registration website allowing

you to plan which roundtable you can impact the

most!

We look forward to engaging with you!

Register

here using the password: Mtg2018.

|

| March 2018 |

- What's New for ComplianceOne® mortgage

- Take Advantage of a Complimentary Quick Start to

What’s New?

-

Get up and running quickly with our overview of

the ComplianceOne mortgage changes so you know

what to expect in our next release. Attend a

complimentary “What’s New” webinar, hosted by our

experienced software trainers. For available dates

and times, and to register, sign-in on our Support

website, and navigate to your ComplianceOne

mortgage product page.

- Click to review What's New with the

Documents

- Click to review the Document

List

- New Functionality

- We have added functionality to display

Specific Lender Credits (currently supported)

along with the collection and disclosure of

Generalized Lender Credits. In the application

phase within the Calculating Cash to Close section

on the Calculations page, Specific Lender

Credits, Generalized Lender Credits,

and Lender Credits are available.

- The product rounds all fees Paid By

Lender and sums them. The total is displayed as

Specific Lender Credits.

- Generalized Lender Credits can be

entered.

- The product sums and rounds Specific Lender

Credits and Generalized Lender Credits.

The total is displayed as Lender Credits

which prints on the Loan Estimate.

In the closing phase on the Calculations

page, we have added a Lender Credits section.

Within that section, Specific Lender

Credits, Generalized Lender Credits,

and Lender Credits are available.

- The product sums all fees Paid By

Lender and displays that total as Specific

Lender Credits.

- If Generalized Lender Credits were

entered in the application phase, that amount will

default to the closing phase; otherwise, an amount

can be entered at closing.

- The product sums Specific Lender

Credits and Generalized Lender Credits

and displays that total as Lender Credits.

The lender credits amount is the same figure shown

as Closing Amount within the Lender Credits that

Cannot Decrease section of the Comparison of Loan

Estimate and Closing Disclosure Fees table.

- For existing transactions, the amount

previously calculated for Specific Lender

Credits will be present in the Lender

Credits field and continue to print to

documents accurately. Once the transaction is

recalculated, the field for Specific Lender

Credits and Lender Credits will be

updated.

For additional information on lender

credits, refer to the following questions in the

Calculations>Loan Estimate/Closing Disclosure

section of Help:

- Updates to Existing Functionality

- Previously, for cosigners on the Demographics

page, when an option was selected under Ethnicity

and I do not wish to provide this

information was not selected, when

subsequently visiting the Demographics page,

Ethnicity I do not wish to provide this

information was selected. This has been

corrected. For existing transactions with

cosigners, it is recommended you review the

Demographics page, select the appropriate choice

for Ethnicity I do not wish to provide this

information, and recreate documents if

necessary.

- Some improvements were made to the way credit

score data displays in the Credit Report section

on the Financial Analysis page. The section now

displays in a format that is more consistent with

the other sections on the Financial Analysis page.

In addition, the following changes were made:

- Score Not Available has been relabeled

to N/A and hover text has been added.

- A Risk Based Pricing Notice is required for

this transaction has been relabeled to

Credit Score Used for Risk Based

Pricing.

- Hover text has been added to Credit Score

Used for Risk Based Pricing, Credit Score Used in

Interface, and Use on Notice of Action

Taken to assist users with these options.

- Refresh Bureau has been moved to the

Credit Bureau Name column as an icon. For

more information, refer to the following question

in Help: How do I update a transaction with the latest

information for the Credit Bureaus defined within

Administration?

The behavior of this section and how the

information impacts documents remains unchanged

with this release.

- When 2018 HMDA Rule Applies is selected

on the Loan Definition page, Type of

Purchaser is now defaulted to 0 = Not

applicable when the Action Taken is either

1 = Loan originated or 6 = Purchased loan, but can

be changed as appropriate. Previously, 8 =

Affiliate institution was incorrectly defaulting.

The ability to default Type of Purchaser

from Administration is not currently supported but

if you use templates, this option is available for

you to set a default in Template Maintenance when

2018 HMDA Rule Applies is selected.

- For transactions using a calculations policy

with Disclose the final payment separately for

installment loans selected, the maximum

payment amount in the $10,000 example paragraph of

the Adjustable Rate Mortgage Program or Adjustable

Rate Mortgage Disclosure Conventional documents

has been corrected. Previously, in some

situations, the maximum payment amount disclosed

was based on the separate final payment instead of

the regular periodic payment. For existing

transactions, review, calculate and recreate

documents if necessary.

- User Defined Fees can now be added at

transaction time without entering a User Fee

Name. 'User Defined' will be populated as the

User Fee Name in these cases. Previously,

an error message indicating ‘Object reference not

set to an instance of an object’ displayed when a

User Defined fee was added at transaction time

without a User Fee Name defined.

- Previously, when a borrower paid fee with zero

variance was added in the application phase and

the amount was decreased and the fee was changed

to lender paid in the closing phase, the Print

page displayed the following warning: 'The total

of Lender Paid Fees exceed 0% tolerance.'

On

the Calculations page, Paid By has been added to

the Loan Estimate values in the closing phase and

red text in the Status column will now indicate

when values have been changed from the application

phase.

- When a policy group with a Property Cost

Policy is updated in Administration, the Escrow

Account Type on the Calculations page will now

be updated to reflect the change in both

transactions and templates. Previously, the value

did not change for the Escrow Account

Type.

- On the Service Provider Information page in

Fees, formatting has been added to Phone

Number and Postal Code in the

transaction.

- When a transaction has only one document

policy option or the first document policy is

defaulted to a new transaction, and the Closing

Cost Expiration Date/Time/Time Zone is completed,

the Closing Cost Expiration Date will now

calculate the Closing Cost Expiration Date

on the Calculations Page. Previously, this value

did not calculate until the user refreshed a

document policy on the Loan Definition page.

- The In 5 years amount on the Loan Estimate and

the Total of Payments amount on the Closing

Disclosure have been updated to include fees where

Add To Amount Requested is selected for Collect

As. Previously, these totals only included fees

where Collect As was Cash or Subtract From

Proceeds. For existing transactions, review,

calculate, and recreate documents if

necessary.

- The Adjustable Rate Mortgage Disclosure

Conventional has been updated to disclose the

first payment that will change as a result of the

initial rate hold expiring within the How Your

Payment Can Change section for Fannie Mae and

Freddie Mac transactions. The sum of the

Initial Rate Hold Term plus one is used to

determine the first payment that can change after

the initial rate hold term. For example, if

Initial Rate Hold Term is 36, the

disclosure will include: Your first payment will

be effective with the 37th monthly payment of your

loan. For existing transactions review, calculate,

and recreate documents if necessary.

- On the HMDA Processing page, you can filter by

Organization, Action Taken Date From, Action Taken

Date To, Submitted, and Loan Number. Reviewed has

been added as a filtering option. You can use the

Reviewed option to view transactions that have

been marked as Reviewed.

- On purchase money transactions, the sum of the

Sales Price entered for each real estate

collateral and mobile home collateral is now

correctly included in the total amount that prints

in M. Due to Seller at Closing (Section M) on the

Closing Disclosure document. Previously, the total

amount did not include the Sales Price

entered for the mobile home collateral.

- The following message will now display when

incorrect user credentials are entered when

transferring a transaction from ComplianceOne

lending or ARTA Lending. Previously, a (500)

Internal Server Error message displayed.

"Login

was unsuccessful. Please correct the errors and

try again. Potential errors could be the

following: Incorrect login information. Password

has expired. User ID is locked. System date and

time are out of sync. If problems persist, please

contact your system administrator. Description:

Inner Exception: ComplianceOne mortgage

transfer."

- All licensed interfaces will now be displayed

in the menu without limitation. Previously, the

number of interfaces that would display was

limited to 20.

- What's New for Interfaces

-

New Features

This release does not include new interface

features.

Updates to Existing Functionality

-

- The Name and Version of the Credit Scoring

Model now prints to the HMDA LAR Preview Report

with the data for the Credit Report designated as

Credit Score Used in Interface on the

Financial Analysis page. Previously, blank was

printing.

- The Credit Score now prints to the HMDA LAR

Preview Report with the data for the Credit Report

designated as Credit Score Used in

Interface on the Financial Analysis page.

Previously, blank was printing.

- The races of the borrower or co-borrower now

display on the CRA Wiz 2017 preview page and in

the .csv file in sequential order when the races

are selected. Previously, they did not display

sequentially.

- Chat with ComplianceOne® mortgage Team

-

Thank you for all the feedback that you have

provided through our Chat with ComplianceOne

mortgage sessions. Your feedback is very

beneficial to our continued approach with

ComplianceOne mortgage. We appreciate any time

that you have shared with us in the past, and look

forward to having you share your feedback in the

future. At this time, we are working at delivering

HMDA to you, so we will be taking a short break

from these events. We will return in early 2018.

Watch for more information to come.

|

| February 2018 |

- What's New for ComplianceOne® mortgage

- Take Advantage of a Complimentary Quick Start to

What’s New?

-

Get up and running quickly with our overview of

the ComplianceOne mortgage changes so you know

what to expect in our next release. Attend a

complimentary “What’s New” webinar, hosted by our

experienced software trainers. For available dates

and times, and to register, sign-in on our Support

website, and navigate to your ComplianceOne

mortgage product page.

- Click to review What's New with the

Documents

- Click to review the Document

List

- New Functionality

This release does not

include new functionality.

- Updates to Existing Functionality

- When 2018 HMDA Rule Applies is selected

on the Loan Definition page, the following updates

have been made to the Preview Report when

Preview LAR Record is selected:

- When Action Taken in the Underwriting

Information Section of the Calculations page is

any of the following; 1 = Loan originated, 2 =

Application approved but not accepted, 4 =

Application withdrawn by applicant, 5 = File

closed for incompleteness, 6 = Purchased loan, or

8 = Preapproval request approved but not accepted,

then 10 = Not Applicable now prints to the Denial

Reason on the Preview Report. Previously, nothing

was printing for the Denial Reason.

- When Action Taken in the Underwriting

Information Section of the Calculations page is 1

= Loan Originated or 6 = Loan Purchased and one of

the following scenarios below applies, 3 = Not

Applicable now prints to the Preview Report:

- Occupancy Status is blank,

Borrower’s Principal Dwelling is not

selected, and Owner’s Principal Dwelling is

not selected for the Reported Real Estate

collateral.

- Occupancy Status is not the Primary

Residence for the Reported Real Estate

collateral.

- On Loan Definition, Construction Note

Type is Construction and Construction

Type is Initial.

- When Action Taken in the Underwriting

Information Section of the Calculations page is 1

= Loan Originated or 6 = Loan Purchased,

Occupancy Status is Primary Residence,

Construction Type is not Initial, and

Reg Z Section 32 Applies is selected on the

Document Data page, 1 = High-cost mortgage prints

to the HOEPA Status on the Preview Report. When

Reg Z Section 32 Applies is not selected in

this scenario, 2 = Not a high-cost mortgage prints

to the HOEPA Status on the Preview Report.

- When Action Taken in the Underwriting

Information Section of the Calculations page is

not 1 = Loan Originated or 6 = Loan Purchased, 3 =

Not Applicable now prints to the HOEPA Status on

the Preview Report.

Previously, in all of the above cases, 1 =

High-cost mortgage or 2 = Not a High-cost mortgage

were printing, depending on the Reg Z Section

32 Applies selection on the Document Data

page.

- Previously, when the rate spread could not be

calculated due to the HMDA Wiz service technical

issues, the HMDA Preview page was not accessible

in ComplianceOne mortgage. This has been resolved.

- Previously, Revocable Trust was

available on the Document Data page within the

Owner section when the collateral owner was a

Trust (not including Illinois Land Trusts) and

Type of Mortgage was Fannie Mae or FHA.

Revocable Trust was also available within

document data entry for the Authorization document

when any Owner, Borrower, Cosigner, and Guarantor

was a Trust (not including Illinois Land Trusts).

Revocable trusts or inter vivos trusts are the

only trust types currently supported in

ComplianceOne mortgage. As a result, we have

removed Revocable Trust from document data

and will set it behind the scenes for any Owner,

Borrower, Cosigner, and Guarantor that is a trust