Why are Cash to Close numbers on the Loan Estimate/Closing Disclosure and the URLA (Qualifying the Borrower) different?

There are different laws/rules that apply to the Loan Estimate and Closing Disclosure versus the URLA.

Even though Cash to Close information is used in sections of the Loan Estimate,

Closing Disclosure, and URLA, different rules apply to calculations and how fields

are populated on the Loan Estimate and Closing Disclosure versus the URLA.

Different agencies define the rules for calculation on these documents:

- The CFPB determines the rules to properly calculate and populate data fields on the Loan Estimate and Closing Disclosure.

- Fannie Mae and Freddie Mac determine the rules to properly calculate and populate data fields on the URLA.

As a result, it is possible to have a different dollar amount value populated in a similarly labeled data field when you compare the Loan Estimate, Closing Disclosure, and URLA forms. The Loan Estimate, Closing Disclosure, and URLA should be as three separate documents that are driven by unique disclosure requirements on how to properly calculate and populate the data fields in them.

Example: A Seller transaction includes the following data:

- Collateral Sales Price - $90,,000

- Loan Amount - $100,000

- Liabilities - Credit Card to be paid off - $5000

- Loan Discounts - 0.6 % of Loan Amount paid by Borrower to Lender, 1.2 % of Loan Amount paid by Seller to Lender

This data results in:

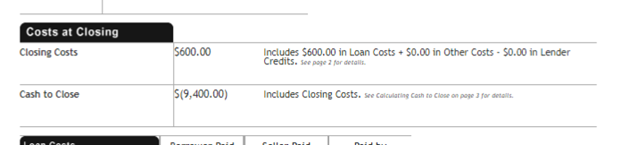

- Cash to Close on the Closing Disclosure is calculated in the following

way: $90,000 (Sales Price) + $600 (Loan Discount paid by Borrower) -

$10,0000 (Loan Amount) =- $9,400

- Cash to Close in Lender Loan Information is calculated in the following

way: $90000 (Sales Price) + $600 (Loan Discount paid by Borrower) +

$5000(Credit Cards) - $100000 (Loan Amount) - 1200 (Loan Discount paid

by Seller)= -$5600