Certifications

As we pointed out in the introduction, you are required to backup withhold if the payee fails to supply a TIN “in the manner required” or if the payee fails to certify that he or she is not subject to backup withholding due to underreporting interest income. [26 USC 3406(a)(1)(A) and (D)] IRS regulations specify the required “manner” in which the payee must supply the TIN. The payee must supply a TIN and certify, under penalties of perjury, that the TIN is the payee’s correct TIN. [26 CFR 31.3406(d)-1(b)(3)] If the payee does not supply the TIN and certify its correctness, or if the payee does not certify that he or she is not subject to backup withholding due to underreporting interest income, you must immediately impose backup withholding on the account. [26 USC 3406(a)(1)(A) and (D)] (We review several exceptions to this rule later in the chapter.)

That you obtain these certifications is part of your general obligation to backup withhold when required. But the “due diligence” standard also requires the payor to obtain a TIN, certified under penalties of perjury, from the payee. [26 CFR 35a.9999-3, Q&A 51] The “reasonable cause” standard makes it advisable for a payor to solicit a TIN from the payee, but does not dictate that the payor require the payee to certify the correctness of the TIN under penalties of perjury. This is perhaps a good time to summarize exactly what the “reasonable cause” standard is.

- That the person “acted in a responsible manner” both before and after the failure occurred, and

- That one of the following is true:

- There are “significant mitigating factors” for the failure, OR

- The failure arose from “events beyond the person’s control.”

[26 CFR 301.6724-1(a)(2)]

- Exercises reasonable care, or that standard of care that a reasonably prudent person would use under the circumstances in the course of its business in determining its filing obligations and in handling account information such as account numbers and balances, and

- Takes significant steps to avoid or mitigate the failure (e.g., requesting extensions of time to file, attempting to prevent the failure if it was foreseeable, acting to remove the cause of the failure once it has occurred, and rectifying the failure as promptly as possible once the failure is discovered).

[26 CFR 301.6724-1(d)]

- The fact that prior to the failure the person was never required to file the particular type of return or statement to which the failure relates (e.g., a payor was never previously required to file 1099 forms);

- The fact that the person has a history of complying with the requirement to which the failure relates, or that the person’s compliance performance has been improving over the years.

- The unavailability of business records.

- Undue economic hardship related to filing on magnetic media.

- Reliance on erroneous information from the IRS.

- Failure caused by an agent of the payor.

- Actions of the payee.

[26 CFR 301.6724-1(c)]

How is it that these rules make it advisable for a payor to solicit the payee’s TIN? When a payor files a 1099 that is missing the payee’s TIN or has an incorrect payee TIN, the payor will most likely argue that the failure was caused by an “event beyond the payor’s control”—namely, an action of the payee (example “5.” above—either the payee supplied no TIN at all or supplied an incorrect TIN). The IRS regulations provide that if the payor makes this argument, the payor must have followed certain solicitation procedures in order to say that it acted “in a responsible manner.” Specifically, the payor must solicit the payee’s TIN at the time of account opening and may have to make two annual solicitations. [26 CFR 301.6724-1(c)(6), (d)(2), (e), and (f)]

The account-opening solicitation under the “reasonable cause” standard is simply a solicitation—nothing more. The regulations state that you only need to request the payee to furnish a correct TIN. [26 CFR 301.6724-1(e)(1)(i)]

The requirements for the annual solicitations are much more detailed. [26 CFR 301.6724-1(e)(1)(ii) – (vi)] We review them at length in the later chapter in this manual having to do with your ongoing backup withholding duties.

The point of all this is that the “reasonable cause” standard makes it advisable for a payor to solicit the payee’s TIN at account opening. You need not require the payee to certify the correctness of that TIN under penalties of perjury in order to meet the “reasonable cause” standard. However, you do need to get that certification in order to avoid immediately beginning backup withholding against interest payments to the account. [26 CFR 31.3406(d)-1(b)(3)] In short, get the certification.

So, to summarize, you must, at account opening: (1) obtain a certified TIN from the payee and (2) have the payee certify that he or she is not subject to backup withholding due to underreporting of interest income.

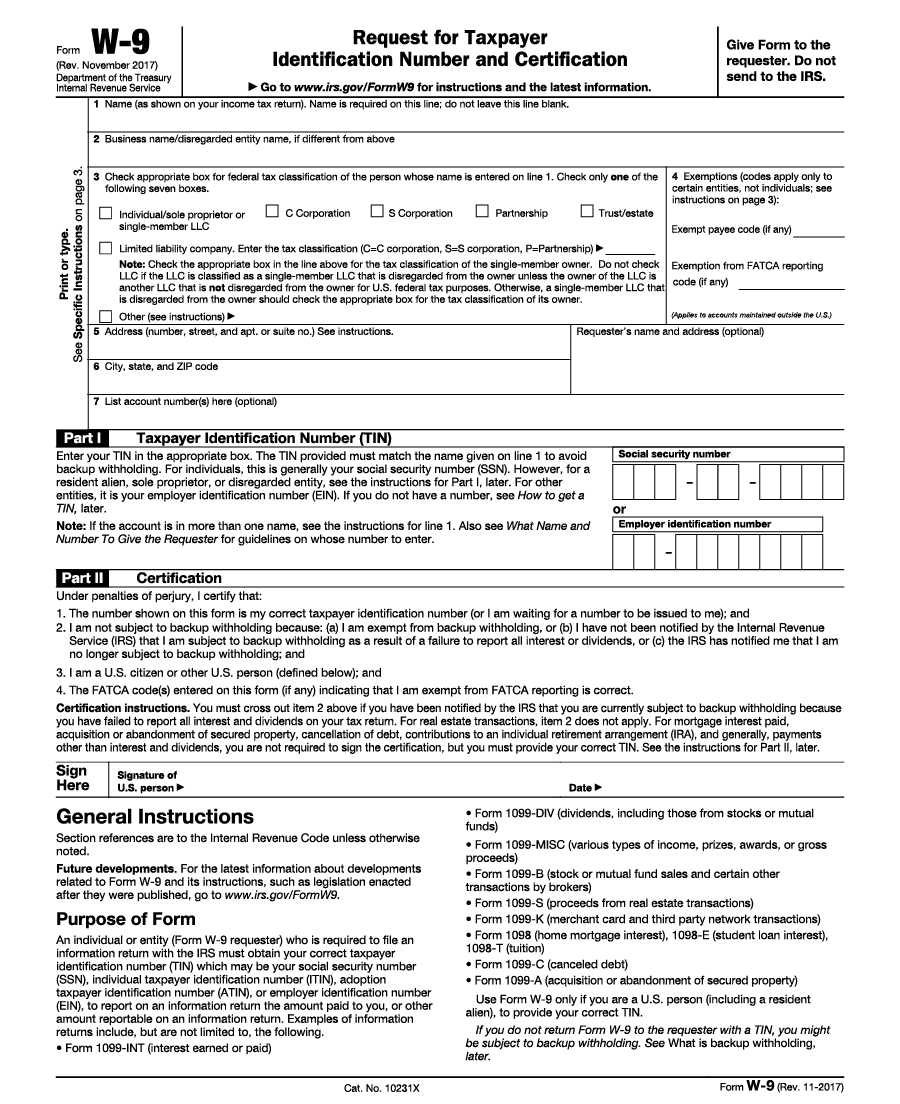

The IRS has an official form for collecting these certifications, Form W-9, shown on the next page. However, the regulations do permit you to use substitute forms to take the certifications. Most financial institutions use a substitute form because they can incorporate the substitute certification language onto their signature cards or other account-opening documents. IRS regulations permit this, and it may be more convenient for you than using a separate W-9 form. The language you should use on a substitute W-9 form used at account opening must be substantially similar to the language on the official W-9. [26 CFR 31.3406(h)-3(c)(1)] The original backup withholding regulations (those in effect before an update in December 1995) provided the following specific language: “Under penalties of perjury, I certify (1) that the number shown on this form is my correct taxpayer identification number and (2) that I am not subject to backup withholding either because I have not been notified that I am subject to backup withholding as a result of a failure to report all interest or dividends, or the Internal Revenue Service has notified me that I am no longer subject to backup withholding.” [26 CFR 35a.9999-1, Q&A 36]