How to test a loan against the Revised General QM definition?

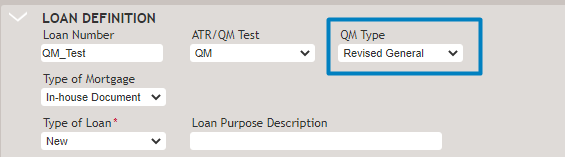

The Revised General QM definition is available in the QM Type field on the Loan

Definition page. If this option is selected, the loan will be tested against the updated

General QM definition.

Note:

In the September 2023 release, the

General QM definitin (General Qualified Mortgage QM rule type) for new

transactions was deprecated. The option to select the General QM on the

Loan Definition page is no longer available and policies were updated to

now use the Revised General QM option.

- Select the Revised General option on the Loan Definition page to use the updated

General QM definition.

- After completing the required fields, select ATR/HOEPA/HPML/QM in the Services Menu to go to the Interface page.

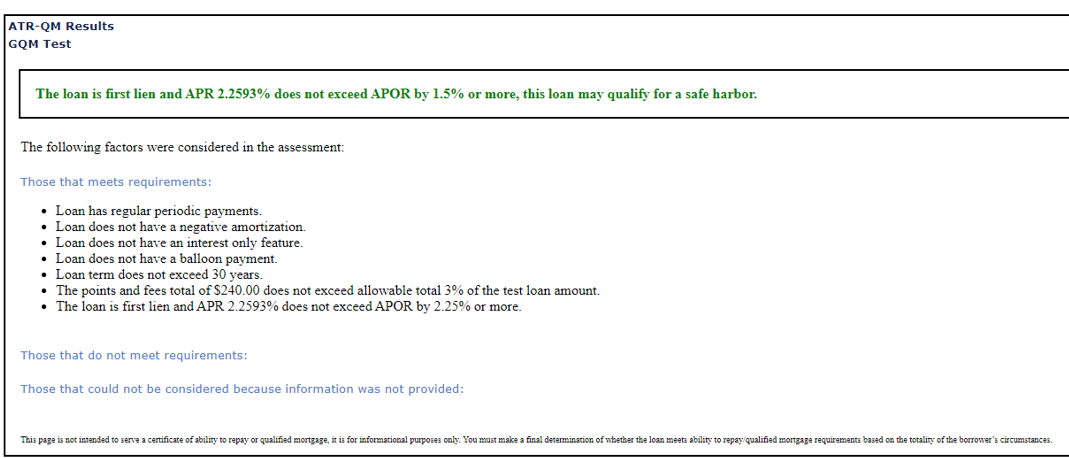

- After you select the Get Lending Analysis Report button, the Wiz Sentinel report

will be generated. The QM section will reflect the 2021 rule update (i.e.

DTI related information will no longer be shown on the report).

- For the ARM loans where the interest rate can change during the first five years of the loan, the APR will be calculated based on the maximum interest rate that may apply during that five-year period as the interest rate for the full term of the loan. This specific APR will be used for the revised General QM purposes only.

- If the loan is fixed rate and first lien, the system will print the following additional language on the Wiz Sentinel report stating that the loan can potentially qualify for Seasoned QM: ‘In addition, this loan satisfies some of the criteria necessary for designation as a Seasoned QM. Final designation of Seasoned QM status cannot be determined until all post-closing performance and portfolio requirements are met.'

If you are interested in learning more about the Revised General QM, please visit

the following resources:

- CFPB Small entity compliance guide

- CFPB ATR-QM comparison chart

- CFPB Executive summary of December 2020 final rule

- Fannie Mae Lender Letter 2021-09

- Freddie Mac Lender Letter 2021-13

Note:

Beginning July 1, 2021, creditors had the option to use

either the General QM definition or the revised, price-based (Revised) General QM

definition. Effective in October 2022, the General QM definition began to be phased

out and was removed as an option in the September 2023 release.