The Loan Payments section (below) is part of the Loan Information screen, viewable when

you select LOAN INFORMATION from the submenu.

| Feature | Description |

|---|---|

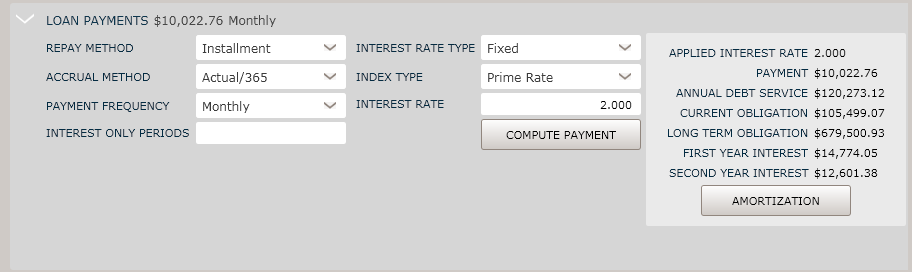

| Repay Method | You can select from the following options:

|

| Repay Method (cont'd) |

|

| Accrual Method | The Accrual Method is used by investors for counting the number

of days in each month and in the year. It is used in the calculation

of the amount of interest payable. Options include:

|

| Payment Frequency | The Payment Frequency is used to determine how often the payment

will be made. Options include:

|

| Interest Only Periods | Interest only payments is when the borrower agrees to pay the

minimum monthly due (interest) for a limited number of

periods. Any amount of interest only periods can be entered, ranging from 0-999 |

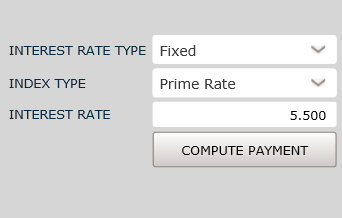

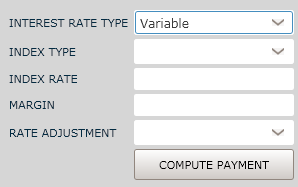

| Interest Rate Type | By SBA definition, a fixed rate loan is one that bears the same

interest rate for the entire term of the loan. A variable rate loan

is one where the interest charged, over the life of the loan, may

vary in accordance with an index. Options are:

|

| Interest Rate | Interest Rate only appears when the Interest Rate Type chosen is “Fixed” Rate. |

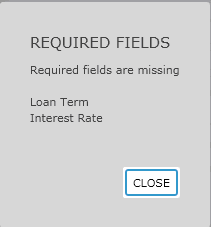

| COMPUTE PAYMENT | Click COMPUTE PAYMENT to compute the Payment, Annual Debt Service, Current Obligation,

Long Term Obligation, First Year Interest and Second Year

Interest based on the criteria previously entered.

Note: Anytime

information changes in Use of Proceeds, Loan Term or items

in the Loan Payment section, you will need to click

COMPUTE PAYMENT again to recompute the values

based on the new changes.

In order for a Payment to be computed, a Loan Term, Use of

Proceeds and Interest Rate must be entered. If one of these

variables is not entered, a message is displayed detailing what

items are missing, as shown in the following example. |

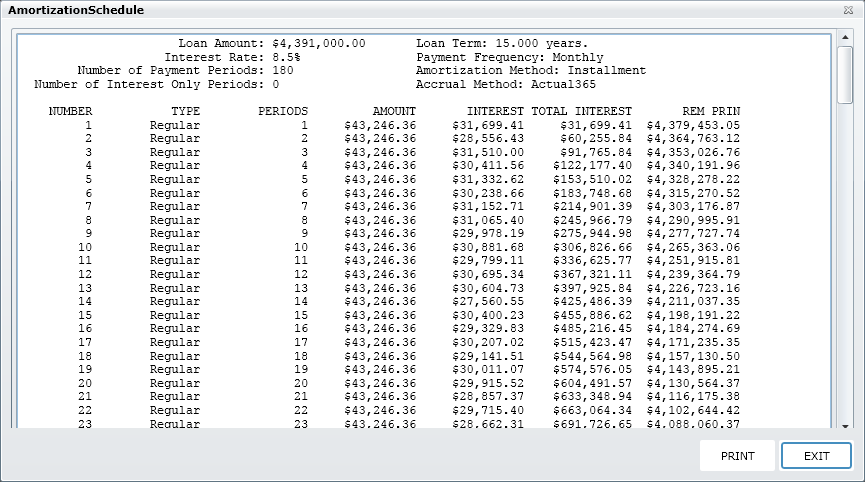

| AMORTIZATION | An amortization schedule is a table that shows the periodic

payment, interest and principal requirements, and unpaid loan

balance for each period of the life of a loan. Click the

AMORTIZATION button to view the Amortization Schedule

window. |